April 2026 – Residential Rental Market Executive Summary

Prepared by: Re/Max Performance Realty Ltd. Property Management

Data Sources: liv.rent · Zumper · Door Insight · Rentals.ca · CMHC · BC Gov

Surrey, British Columbia

April 2026 marks a meaningful inflection in Surrey’s residential rental market. After months of broad-based decline, the data is beginning to differentiate: smaller-format condos continue to soften, while family-sized segments are showing early signs of stabilisation. The overall Surrey rental median stands at $1,950/month, down 9% year-over-year but up 2% month-over month — the first positive MoM reading across the full market in several months (Zumper April 2026).

The one-bedroom condo market remains the most pressured segment. Surrey City Centre’s average 1BD has fallen to $1,707 — a 10% annual decline — as the city absorbs the tail end of a record purpose-built pipeline heavily weighted toward small-format units. The two-bedroom segment, however, is showing genuine absorption strength, with the fastest relative YoY movement at -4.5% but consistent DOM and active demand from couples, small families, and shared households. Three-bedroom condos have stabilised at $2,325 median following February and March repricing.

The report expands this month to cover five bedroom categories for the first time. The four-bedroom and five- bedroom segments — primarily detached houses and larger townhouses — are showing positive month-over- month momentum (+1.5% and +2% respectively), driven by family-format demand that was never displaced by the condo oversupply cycle. Five-bedroom homes are tracked for the first time this month at a median of $4,200.

Surrey remains Metro Vancouver’s most affordable rental city at $2.05 per square foot (liv.rent April 2026). Greater Vancouver vacancy holds at 3.7% — the highest since 1988. Move-in incentives remain widespread. The structural demand base — 600,000+ residents, the fastest-growing city in BC, institutional anchors at SFU Surrey and the planned UBC campus — is intact and will reassert itself as the supply cycle concludes.

Key findings from April 2026 data (liv.rent, Zumper, Door Insight, Rentals.ca/Point2Homes):

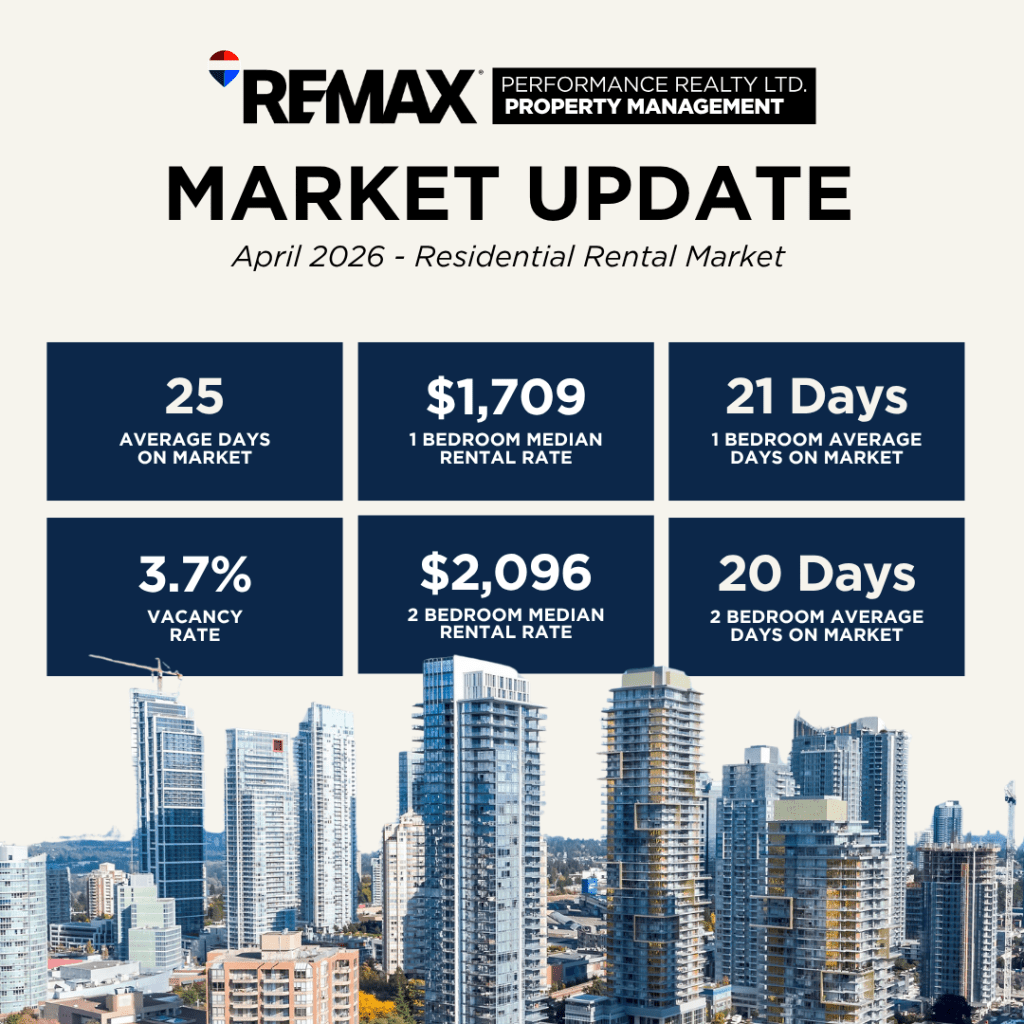

- 1BD condo median: $1,709 — down 9% YoY, up 2% MoM. Surrey City Centre 1BD average fell to $1,707 (-10% YoY). New builds competing aggressively on price.

- 2BD condo median: $2,096 — down 4.5% YoY, -5.6% MoM. The most actively demanded condo format. Furnished 2BD averages $2,155. Absorption rate fastest in the condo stack.

- 3BD condo median: $2,325 — down 3.3% YoY, effectively flat MoM following February and March’s sharp repricing. Townhouse format still commands premium at $2,850.

- 4BD (TH/House) median: $3,400 — down just 2% YoY, +1.5% MoM. Detached houses dominate; Newton and Cloverdale anchor floor at $2,800, South Surrey premium at $4,000+.

- 5BD House median: $4,200 (new segment, April 2026 baseline). Range $3,500–$5,500. Multi- generational household demand anchors floor pricing. Average DOM 30 days.

MEDIAN ASKING PRICES

April 2026 rental data is sourced from liv.rent (April 2026 Metro Vancouver report), Zumper April 2026 Rent Research, Door Insight March 2026, and active Rentals.ca / Point2Homes listings for the 4BD and 5BD segments. This is the first month in which five bedroom categories are tracked, providing a full picture from entry- level condo to large detached house rental. All figures are asking rents. Effective rents are lower where move-in incentives apply — typically 8–17% annualised reduction for a one-month free arrangement, which remains common across Surrey.

The April data reinforces a two-speed market. The condo stack (1BD through 3BD) is still working through oversupply, with YoY declines of 3–9% depending on segment. The family-format stack (3BD townhouse, 4BD, and 5BD) is stabilising or improving month over-month, as this supply has never been as oversupplied as the condo pipeline and the demand base — multi-generational households and families — is structurally undersupplied relative to need.

| UNIT TYPE | MEDIAN/MO. | MINIMUM | MAXIMUM | AVERAGE DOM |

| 1 Bed / 1 Bath – Condo | $1,709 | $1,200 | $2,100 | 21 days |

| 2 Bed / 1–2 Bath – Condo | $2,096 | $2,155 | $2,800 | 20 days |

| 3 Bed / 1+ Bath – Condo | $2,325 | $2,000 | $2,800 | 25 days |

| 3 Bed / 2+ Bath – Townhouse | $2,850 | $2,400 | $3,300 | 20 days |

| 4 Bed / 2+ Bath – Townhouse | $3,400 | $2,800 | $4,500 | 27 days |

| 4+ Bed / 2+ Bath – House | $4,200 | $3,500 | $5,500 | 30 days |

Key Observations

- Surrey’s rental market is now clearly two-speed. The 1BD and 2BD condo segments face the largest YoY declines (-9% and -4.5%), driven by the heaviest concentration of new purpose-built supply. The 3BD–5BD family formats are declining modestly YoY (-1% to -3.3%) or growing MoM, reflecting structural undersupply of family-sized rentals.

- Build year remains the dominant pricing variable in the condo stack. New 2024 2026 builds command $150–$350/month more than equivalent 2000–2015 stock, and 1990s vintage units are being forced to compete on size and price rather than amenity.

- Surrey at $2.05/sq ft is Metro Vancouver’s most affordable rental market — significantly below Langley ($2.63), Burnaby ($3.35), Richmond ($3.25), North Vancouver ($3.71), and Vancouver ($4.05) (liv.rent April 2026).

- The 4BD and 5BD segments are showing positive MoM momentum for the second consecutive month. Newton and Cloverdale offer family homes from $2,800/month. South Surrey and Fleetwood premiums reach $4,000–$4,500 for newer detached product.

- Average days on market remain 20–25 days for well-priced condo units, extending to 27–30 days for larger homes — consistent with previous months. Outliers at 40–50 days in the 3BD condo segment reflect pricing resistance from legacy landlords not acknowledging the market reset.

- Move-in incentives remain standard practice. One month free rent is common across purpose-built buildings in City Centre, Whalley, and Fleetwood. Two months free is available at select newer buildings with elevated vacancy.

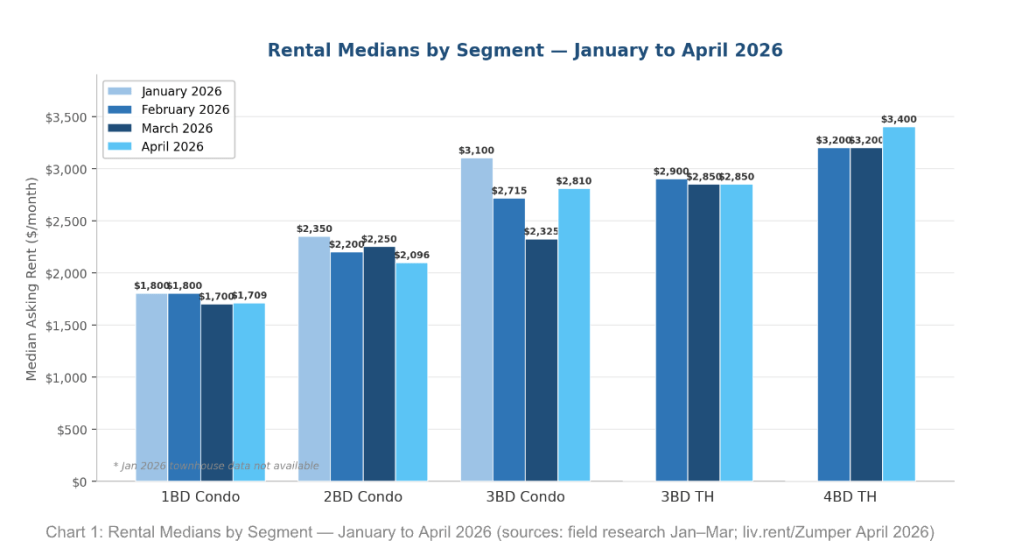

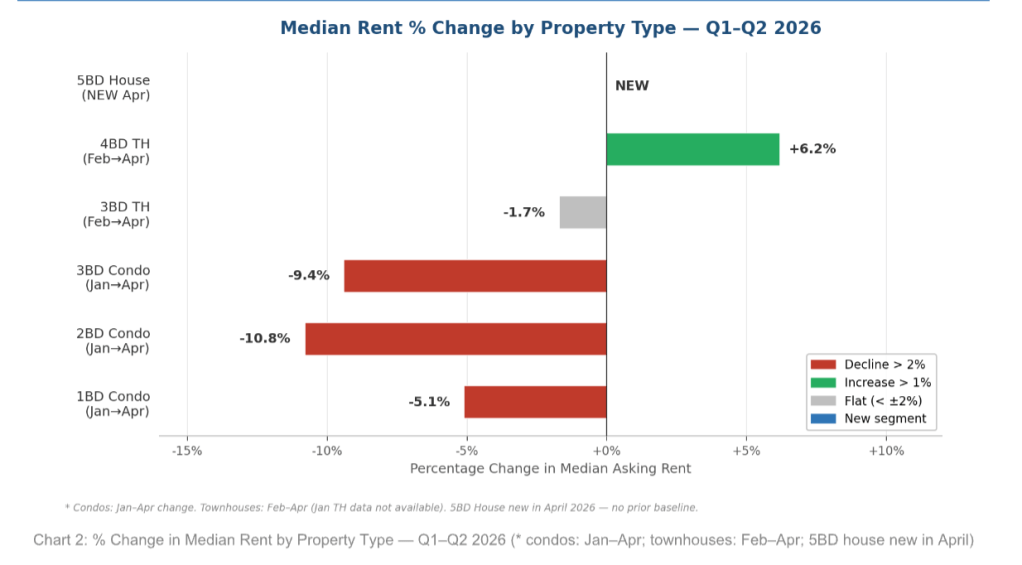

Q1-Q2 2026 Rent Trend Analysis

The two charts below visualise median asking rent movements across all tracked property types from January through April 2026. Chart 1 shows absolute medians by segment. Chart 2 shows percentage change over the full available period — January to April for condo segments, February to April for townhouses where January data was unavailable.

2. SUPPLY

The supply cycle driving Surrey’s rental correction is entering its final phase. The record wave of purpose-built rental completions that pushed Greater Vancouver vacancy to 3.7% is largely delivered; what the market is now absorbing is the pipeline’s tail. The more significant April 2026 dynamic is compositional: the delivered units were disproportionately studio and one-bedroom, and the April data confirms these remain the hardest to place — while family-format supply (3BD TH, 4BD+) was never overbuilt and is tightening.

Developer confidence is deteriorating on net-new starts, driven by three converging pressures: US-Canada tariffs adding 5–15% to construction costs, softening condo presales (the primary financing vehicle for purpose-built construction in Surrey’s market), and cautious lender sentiment. The pipeline for 2028+ delivery is thinner than 2025–2027, which is the structural setup for the eventual rent recovery. The current oversupply is transitional, but the transition is proving longer than initially anticipated — particularly for the small-format units that were most aggressively built.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Metro Vancouver rental completions (2025) | Above 5-yr average | Purpose-built pipeline now largely delivered; absorption lagging. CMHC 2025 |

| Greater Vancouver vacancy ratevacancy rate | 3.7% (Oct 2025) | Highest in 30+ years — more than doubled from 1.6% in CMHC |

| New 2026-vintage units entering market | Repricing pressure | New builds entering at or below existing stock prices in some segments (3BD condo) |

| Rental unit mix mismatch | Studio/1BD heavy | Pipeline skewed to smaller units; demand stronger for 2–3BD family-sized formats |

| Move-in incentives | 1–2 months free | Active across Surrey April 2026 — Craigslist & purpose-built operators confirmed |

| STR units returning to LTR | Ongoing | BC STR Registry Year 2 (Jan 2026): thousands of investor units added to long-term supply |

| Developer new starts | Slowing | Tariff cost pressure + soft presales reducing pipeline for 2028+ delivery |

3. DEMAND

April 2026 demand signals are mixed but directionally improving. The broad softening of 2025 — reduced immigration, elevated youth unemployment, suppressed household formation — remains the dominant backdrop. However, within that softness, the month over-month data is beginning to differentiate. The overall Surrey median ticked up 2% MoM (Zumper April 2026) for the first time since the correction began, suggesting the worst of the demand weakness may be behind us for mid- and large-format units.

The condo market’s 1BD segment remains challenged. Surrey City Centre 1BD fell to $1,707 average — reflecting both the heaviest concentration of new supply and the most sensitive demand pool (students, young singles, new arrivals) to immigration policy changes. The 2BD segment’s -5.6% MoM reading is technically negative but reflects active absorption — the demand for two-bedroom formats from couples, shared households, and small families is genuine and ongoing, with DOM remaining tight.

The 4BD and 5BD segments’ positive MoM performance tells a different demand story: multi-generational families, who were never the primary target of the condo pipeline, are actively seeking larger homes and finding value in Surrey’s detached rental market at a substantial discount to ownership costs. This demand is structural and will not disappear with the immigration cycle.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Surrey Population | 600,000+ (BC’s fastest growing) | City of Surrey 2025. Structural long-term demand base |

| Immigration levels | Federal cuts 2025-2027 | Non-permanent resident outflow softening 1BD demand most. CMHC 2025 |

| Surrey YoY rent change (all) | 9% (Zumper Apr 2026) | Overall market median down 9% YoY. +2% MoM signal demand stabilising |

| Surrey 1BD median | $1,709/mo (Apr 2026) | liv.rent April 2026 — down from $1,903 in City Centre a year ago |

| Surrey $/sq ft | $2.05 (Apr 2026) | Lowest in Metro Vancouver. liv.rent April 2026 |

| 2BD segment | Most in-demand condo type | Fastest MoM: -5.6% reflects active absorption by couples & small families |

| 4–5BD segment | MoM positive trend | +1.5% to +2% MoM in April: family-format demand recovering. Rentals.ca Apr 2026 |

| Tenant negotiating power | Strongest in a decade | Vacancy above 3.7%, incentives widespread; renter’s market since 1988 |

4. FUEL

The capital environment in April 2026 continues its gradual improvement for the rental sector, though the benefits are distributed unevenly. For existing landlords, lower Bank of Canada rates are reducing carry costs on variable-rate mortgages — providing some relief to investor-condo owners facing declining rents. For tenants, the rate reductions have meaningfully improved mortgage affordability at the margin, but the gap between renting and ownership remains wide for most Surrey households; the primary effect is modest movement of some financially stronger renters into entry-level ownership, which partially relieves demand.

For developers, the picture is more complicated. The policy levers — PTT exemption, CMHC MLI Select, federal Apartment Construction Loan Program — remain active and effective for projects already in the pipeline. However, US-Canada tariff costs (5–15% on steel, aluminum, and lumber) are materially impacting feasibility for new projects breaking ground in 2026. The BC Rent Cap at 2.3% for 2026 — below current inflation in some cost categories — further compresses operating margins, discouraging speculative new supply. Net result: the current supply wave delivers through 2026–2027, then the pipeline thins materially, setting up the conditions for rent recovery.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Bank of Canada policy rate | 2.25% (Oct 2025) | Further cuts anticipated into 2026; improving landlord carry costs |

| Impact on renters | Mixed | Lower rates improve homebuying affordability marginally; most renters still locked out |

| BC Property Transfer Tax exemption | In effect Jan 2025–Dec 2030 | Purpose-built rental buildings exempt from PTT; stimulating supply-side activity |

| Federal Rental Construction Financing | Active (RCFi / MLI Select) | CMHC low-interest loans for rental construction; active in Surrey |

| Construction cost environment | Elevated (+5–15%) | US–Canada tariffs on steel, aluminum, lumber. Constraining new starts. CMHC 2025 |

| Developer confidence | Softening for new starts | Condo presales down significantly — forward indicator of 2028+ supply tightening |

| BC Rent Increase Guideline 2026 | 2.3% cap | Most landlords not exercising full cap — vacancy risk outweighs rental upside |

| City of Surrey permitting | 75% faster (2025) | $35.1M invested in housing; digital improvements reducing developer timelines |

PEESTEL FACTORS

The following Political, Economic, Environmental, Social, Technological and Legal factors are shaping the Surrey residential rental market as of April 2026. Several dynamics have evolved since March: the federal election has concluded, immigration levels remain below prior norms, and the first April 2026 data points confirm the MoM recovery trend in overall median rents alongside continued YoY pressure on smaller condo formats.

| POLITICAL | Federal election concluded. Housing affordability remains a top policy priority. Federal immigration cap (2025–2027) is the primary near-term demand headwind — most NPRs are renters. BC government citing rising vacancy as policy success. STR Registry Year 2 (Jan 2026) returning investor-held units to long-term market. City of Surrey’s $35.1M housing investment and OCP update underway. Bill 44 upzoning near SkyTrain stations taking effect. |

| ECONOMIC | Bank of Canada rate at 2.25%; further cuts expected through 2026. BC GDP growth ~1.1% in 2026 — modest. Youth unemployment still elevated, suppressing household formation. US–Canada tariffs (+5–15% construction costs) constraining new rental starts. Surrey at $2.05/sq ft remains Metro Vancouver’s most affordable rental market (liv.rent Apr 2026). Overall Surrey median $1,950/mo, down 9% YoY (Zumper Apr 2026). |

| ENVIRONMENTAL | BC Energy Step Code and heat pump mandates raising new construction costs but reducing tenant utility bills. New 2024–2026 stock significantly more energy-efficient. Flood risk in South Surrey and Newton affecting insurance premiums. Climate disclosure requirements increasingly factored into institutional rental development decisions. |

| SOCIAL | Surrey’s population exceeds 600,000 — BC’s fastest-growing city. Younger, more diverse demographic base drives disproportionate demand for 2–4 bedroom family-format units. Rising affordability pressure pushing households toward shared living, increasing demand for 3+ bedroom formats. BC Housing waitlist in Surrey elevated. Non-market supply pipeline active but insufficient to address core housing need at bottom of income distribution. |

| TECHNOLOGICAL | Facebook Marketplace and Craigslist dominate for private landlord and investor-condo listings. Purpose-built operators use Zumper, Rentals.ca, liv.rent, and Apartments.com. April 2026 data sourced from liv.rent, Zumper, Door Insight, and Rentals.ca/Point2Homes. New 2024–2026 purpose-built buildings feature smart home tech, app-based amenity booking, keyless entry, and EV charging — commanding a premium. Surrey’s digital permitting portal reducing approval timelines.timelines. |

| LEGAL | BC Residential Tenancy Act: strict eviction rules, fixed-term rollover, 2.3% rent cap (2026). Most landlords not exercising full cap — vacancy risk too high. Bill 44: small-scale multi-unit zoning near SkyTrain — gentle density unlocking over 3–5 years. BC STR Registry Year 2 (Jan 2026) returning illegally operated units to LTR market. PTT exemption (Jan 2025 Dec 2030) and CMHC MLI Select are the two most impactful instruments stimulating new rental supply in Surrey. |

MARKET OUTLOOK

Near-Term: 0–12 Months (Renter’s Market, Differentiating)

Surrey will remain a renter’s market through 2026, but the monolithic decline of 2024 2025 is giving way to a more nuanced picture. The 1BD condo market still has supply to absorb and YoY declines will persist. The 2BD and 3BD condo markets are approaching floor conditions — the September 2025 to March 2026 repricing has brought them within range of genuine market-clearing levels, and April’s stabilisation signals the correction may be in its final innings for these segments. Family-format rentals (3BD TH, 4BD+) are already showing positive MoM momentum and are unlikely to decline further absent a significant new shock. Move-in incentives will persist through Q3 2026 in the purpose built condo sector but will begin to fade in the family-format segments.

Medium-Term: 1–3 Years (Rebalancing on a New Floor)

The 2027–2028 period will see vacancy return toward equilibrium (approximately 3%) as the purpose-built pipeline thins, immigration levels stabilise, and delayed household formation unwinds. Rent recovery will be gradual — the market is rebalancing to a floor below 2022–2023 peaks, not returning to them. The segments most likely to lead the recovery are 3BD townhouses (structurally undersupplied, family-demand anchored), followed by 4BD and 5BD houses. The 1BD condo market will be last to recover given the depth of oversupply and the ongoing mismatch between supply mix and effective demand. Surrey’s cost advantage ($2.05/sq ft vs Vancouver’s $4.05) provides a structural demand magnet that will amplify recovery speed once the cycle turns.

Structural Fundamentals (Intact and Strengthening)

Surrey’s long-term rental demand thesis is among the strongest in Canada. A population exceeding 600,000, the fastest municipal growth rate in BC, a young and diverse demographic profile, multi-generational household culture driving sustained demand for 2–5 bedroom formats, and institutional demand anchors at SFU Surrey and the incoming UBC campus — all point to durable, long-horizon rental need. The current correction is a supply- demand timing mismatch amplified by a federal immigration reset. It is not a structural market failure. The most acute unmet need at the bottom of the market — units affordable to lower-income households — remains entirely unaddressed by the current pipeline, and will represent the most significant affordability challenge in Surrey’s housing market over the next decade.

DATA SOURCES & METHODOLOGY

April 2026 median asking prices sourced from: liv.rent April 2026 Metro Vancouver Rent Report (1BD $1,709, 2BD $2,096, 3BD $2,810, Surrey City Centre 1BD avg $1,707, Surrey $/sq ft $2.05); Zumper April 2026 Rent Research (overall Surrey median $1,950, -9% YoY, +2% MoM); Door Insight March 2026; Rentals.ca and Point2Homes April 2026 active listings for 4BD and 5BD house-format segments. Market context from: CMHC 2025 Rental Market Report (December 12, 2025) — Greater Vancouver vacancy 3.7%, highest since early 1990s; CMHC 2025 Mid-Year Rental Market Update (July 2025); BC Government Housing Minister statements (November–December 2025); Rentals.ca October 2025 National Rent Report; Bank of Canada policy rate announcements. January–March comparables from Re/Max Performance Realty Ltd. field research (primary comparables). All April 2026 figures are asking rents from publicly reported data sources, not field research comparables. Effective rents may be lower where incentives apply. This report reflects a point-in-time snapshot of April 2026 market conditions.