February 2026 – Residential Rental Market Executive Summary

Surrey, BC | Condos, Townhouses & Houses Rental Market

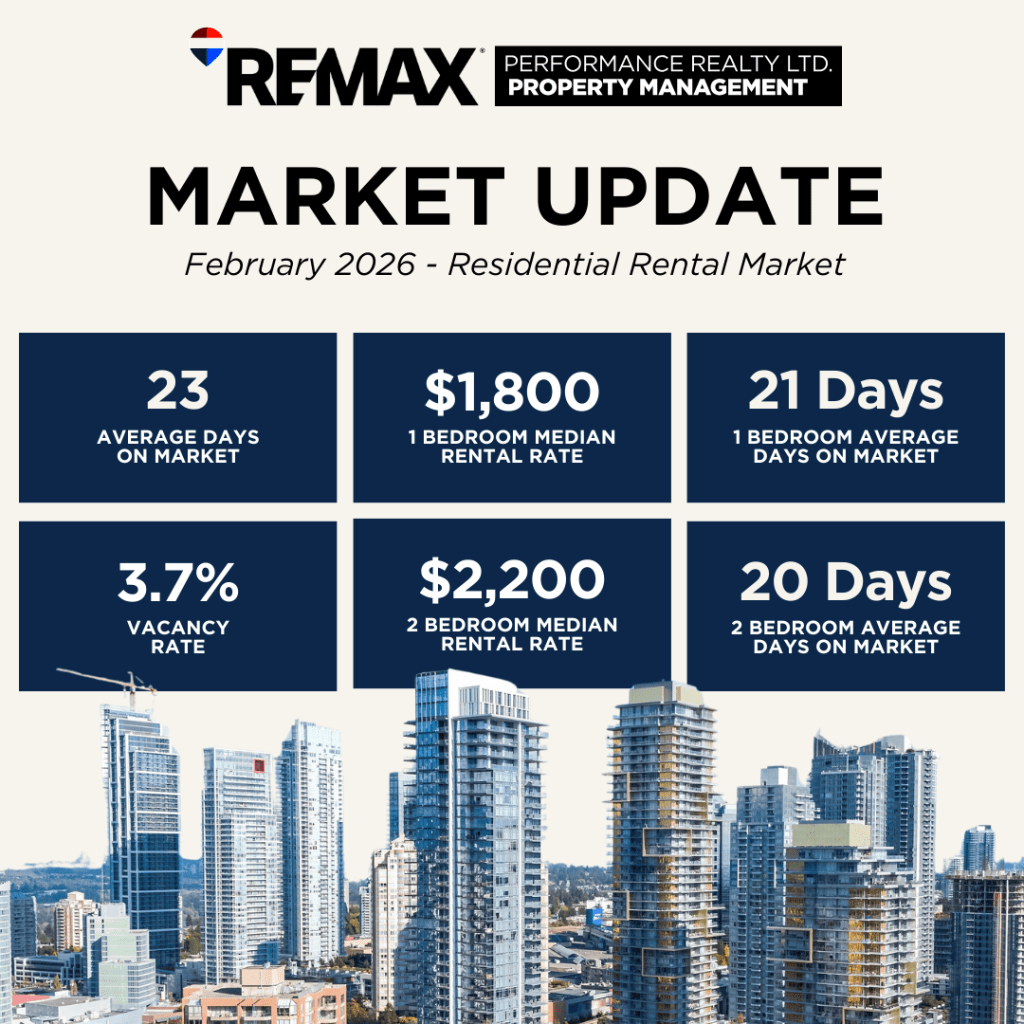

Market Overview by Performance Property Management

Surrey’s residential rental market has undergone a decisive shift in favour of tenants. As of February 2026, the Greater Vancouver vacancy rate has reached 3.7% — the highest in over 30 years — driven by a record pipeline of purpose-built rental completions meeting weaker demand from reduced immigration and a softer job market for young renters. Surrey is specifically named by CMHC as experiencing elevated leasing difficulty, particularly for studio and one-bedroom units.

Asking rents for one-bedroom units in Surrey are down 9.3% year-over-year as of December 2025, with annual declines recorded for 24 consecutive months across BC. Move-in incentives — one to two months free rent, moving allowances, and signing bonuses — are active across the market, confirmed in both CMHC’s annual report and live Craigslist listings reviewed for this report. Despite this cyclical softness, Surrey’s structural demand base remains intact, supported by a population of 600,000+ and ongoing population growth.

| –9.3%Surrey 1BD Rent (YoY)Dec 2025 vs Dec 2024 (BC Gov / Rentals.ca) | 3.7%Greater Van. Vacancy RateHighest in 30+ years — Oct 2025 (CMHC) | $1,800Median 1BD Asking RentYour research median — Feb 2026 comparables | $2,900Median 3BD TH Asking RentYour research median — Feb 2026 comparables |

MEDIAN ASKING PRICES

The median asking rents below are calculated from your primary field research comparables (11 listings per 1BD/2BD segment, 8 for 3BD condo, 11 for 3BD TH, and 7 for 4BD TH), supplemented by 60+ additional Craigslist listings reviewed on February 26, 2026. All figures represent asking rents. Effective rents are lower where move-in incentives apply — typically reducing annualised cost by 8–17% for a one-month free arrangement.

| Unit Type | Median/Mo | Avg/Mo | Min | Max | Avg DOM |

| 1 Bed / 1 Bath — Condo | $1,800 | $1,795 | $1,650 | $1,950 | 21 days |

| 2 Bed / 1–2 Bath — Condo | $2,200 | $2,185 | $1,950 | $2,300 | 20 days |

| 3 Bed / 1+ Bath — Condo | $2,715 | $2,716 | $2,450 | $3,100 | 24 days |

| 3 Bed / 2+ Bath — Townhouse | $2,900 | $2,920 | $2,800 | $3,000 | 20 days |

| 4 Bed / 2+ Bath — Townhouse | $3,200 | $3,271 | $3,000 | $3,700 | 27 days |

Key Observations

- City Centre and Whalley corridor command $150–$400/month premium over comparable units in Fleetwood, Newton, and Guildford across all unit types.

- New 2024–2026 builds consistently achieve $200–$400/month more than equivalent-sized 1990–2010 stock. 1990s Guildford condos (10736 & 10463 150 St) show the widest spread, at $2,450–$2,850 vs $3,100 for a newer City Centre 3BD.

- Days on market are consistent at 13–25 days for well-priced units, with outliers at 40–50 days for overpriced or under-amenitised product. Basement suites and secondary suites (not in your dataset) trade at $1,000–$1,600 for 1BD on Craigslist.

- Craigslist range widens the picture: 1BD from $1,250 (basement InSuite) to $2,120 (new pet-friendly City Centre condo with amenities). The spread reflects quality and format more than location.

- Townhouses are the most consistent segment: 3BD TH range is tight ($2,700–$3,000) with minimal variance by node, confirming strong family-unit demand and limited supply.

SUPPLY

Rental housing supply in Metro Vancouver has reached historically high levels following years of strong purpose-built construction, condo completions, and the return of short-term rental units to the long-term market. This supply surge is the primary driver of rising vacancy and declining asking rents. The pipeline is, however, beginning to slow: developer confidence is softening due to higher construction costs and tariff uncertainty, suggesting the current oversupply condition is transitional rather than structural.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| ── NEW PURPOSE-BUILT SUPPLY | ||

| Metro Vancouver rental completions (2025) | Above 5-yr average | CMHC 2025 Rental Market Report (Dec 2025) — growth higher than 5-year avg; concentrated in City of Vancouver but strong in Surrey too |

| National purpose-built vacancy rate | 3.1% (Oct 2025) | Up from 2.2% (Oct 2024) and record low of 1.5% (2023). CMHC 2025 Rental Market Report |

| Greater Vancouver vacancy rate | 3.7% (Oct 2025) | Highest in 30+ years — more than doubled from 1.6% in 2024. BC Housing Minister statement, Dec 11 2025 |

| Surrey: new stock leasing difficulty | Elevated | CMHC 2025: studio/1BD mix less desirable; heavy competition from condo completions. Vacancies in Surrey expected to remain higher for coming years |

| Rental unit mix problem | Studio/1BD heavy | New purpose-built pipeline skewed to smaller units. Demand stronger for 2–3BD family-sized units; mismatch driving absorption challenges |

| ── INCENTIVES & MARKET SIGNALS | ||

| Move-in incentives | 1–2 months free rent | Active across Surrey — confirmed in Craigslist Feb 2026 (multiple listings), CMHC 2025 mid-year, and CMHC 2025 annual report |

| Landlord behaviour | Competing to fill | Purpose-built operators offering incentives; condo investor owners more willing to lower rents outright. CMHC 2025 |

| Secondary market (condo rentals) | Heavy competition | Investor-owned condos competing with purpose-built. Condo owners prioritise occupancy over cap rates. CMHC 2025 |

| Short-term rental returns | Units returning to LTR | BC STR registry Year 2 (Jan 2026): thousands of units returned to long-term rental market, adding supply |

DEMAND

Rental demand in Surrey faces three concurrent cyclical headwinds: reduced international migration, suppressed youth household formation, and modest conversion of renters into first-time homeowners as mortgage rates decline. These headwinds are real but temporary. Surrey’s structural demand base — anchored by population growth, cultural diversity, and institutional expansion — remains among the strongest in Canada.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| ── POPULATION & DEMOGRAPHICS | ||

| Surrey population | 600,000+ (BC’s fastest growing) | City of Surrey 2025. Structural long-term demand base. Young, diverse, growing |

| Immigration targets reduced | Federal cuts 2025–2027 | Non-permanent resident (NPR) outflow in BC — 3 consecutive quarters. Most NPRs are renters. CMHC 2025 |

| International students | Declining | Federal study permit cap (2024–2025). SFU Surrey and planned UBC campus support local demand but international component shrinking |

| Youth unemployment | Elevated | Slow wage growth and weak youth job market reducing household formation — more young people co-living or staying with parents. CMHC 2025 |

| ── RENT TRENDS | ||

| Surrey 1BD asking rent change | –9.3% YoY (Dec 2025) | BC Housing Minister statement citing Rentals.ca, Dec 8 2025. 24th consecutive month of annual decline in BC |

| Surrey 1BD asking rent change | –11.7% YoY (Sep 2025) | Rentals.ca October 2025 report — Surrey among Canada’s steepest rent declines |

| Surrey 1BD avg asking rent | ~$1,846/mo (Jul 2025) | liv.rent August 2025 Metro Vancouver Rent Report; down 5.8% YoY; most affordable Metro Van. city by $/sf at $2.59 |

| Surrey all-type median | $1,950/mo (Feb 2026) | Zumper Rent Research Feb 2026 — down 11% in last year |

| BC overall asking rent trend | –8.5% over 2 years | BC Housing Minister Dec 2025: ‘BC continues to lead the country in asking-rent declines’ |

| Metro Vancouver 2BR turnover rent | Declined in 2025 | Average 2BD turnover unit rent declined in Vancouver (CMHC 2025) — renter’s market strengthening |

| ── RENTER’S MARKET CONDITIONS | ||

| Tenant turnover rate | Rising | After multi-year lows, turnover increasing. More options + competitive pricing. Renters moving for better deals. CMHC 2025 |

| Negotiating power | Strongest in a decade | Vacancy above 3.7%, incentives widespread, rent declining — clearest renter’s market in Metro Vancouver since 1990s |

| Affordable units | Still very tight | Only 1–2% of units affordable to lower-income households were vacant. CMHC 2025 — affordability crisis persists at bottom of market |

FUEL — COST & ACCESS TO CAPITAL

The Fuel section examines the cost and availability of capital for both rental housing development and tenant access to housing. February 2026 presents a transitional environment: monetary conditions are easing (improving development viability and homebuyer affordability), but construction cost inflation, tariff risk, and cautious lender sentiment are limiting the pace of new rental supply creation.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| ── INTEREST RATES & MONETARY CONDITIONS | ||

| Bank of Canada policy rate | 2.25% (Oct 2025) | Further cuts anticipated into 2026. Improving landlord carry costs and gradually enabling homebuyer conversion from rental market |

| Impact on renters | Mixed | Lower rates improve homebuying affordability for some renters, marginally reducing rental demand. But most renters remain locked out of ownership |

| ── DEVELOPMENT FINANCE | ||

| BC Property Transfer Tax exemption | In effect Jan 2025–Dec 2030 | Purpose-built rental buildings exempt from PTT — meaningful cost reduction for developers. Stimulating supply-side activity |

| Federal Rental Construction Financing Initiative | Active (RCFi / MLI Select) | CMHC low-interest loans for rental construction. MLI Select product adoption grew significantly in 2024. Active in Surrey |

| Construction cost environment | Constrained | US-Canada tariffs on steel, aluminum, lumber adding 5–15% to construction costs. Some projects delayed or cancelled. CMHC Fall 2025 Supply Report |

| Developer confidence | Softening for new starts | Condo presales declined significantly in Vancouver — leading indicator of future secondary rental supply tightening in 3–5 years |

| ── TENANT FINANCIAL CONDITIONS | ||

| Rent-to-income ratio | Still elevated | Despite falling rents, ratio has risen steadily since 2020. Affordability worsened over time even with recent rent declines. CMHC 2025 mid-year |

| Gap: vacant vs occupied units | Significant | New tenants paying more than sitting tenants on average. Large premium still exists on turnover leases. CMHC 2025 |

| BC Rent Increase Guideline | 3.0% cap (2025) | Most same-sample rent increases in 2025 were below the 3% guideline — landlords not exercising full rights. CMHC 2025 |

| City of Surrey permitting | 75% faster (2025) | $35.1M invested in housing initiatives, 20+ process improvements — reducing carrying cost and uncertainty for developers |

PEESTEL FACTORS

The following Political, Economic, Environmental, Social, Technological and Legal factors are shaping the Surrey residential rental market as of February 2026.

| POLITICAL | Federal election year (2025–2026): housing affordability is a top-tier campaign issue across all major parties. Reduced immigration targets (2025–2027) are the single largest near-term driver of demand softening — most non-permanent residents are renters.BC Provincial government actively citing rising vacancy rates as a policy success. Short-term rental registry (Year 2, Jan 2026) returning investor-held units to long-term rental market. BC Builds program targeting middle-income rental housing.City of Surrey approved $35.1 million in housing investments in 2025 (fully grant-funded). OCP update underway to support densification. Bill 44 upzoning near SkyTrain stations. |

| ECONOMIC | Bank of Canada policy rate at 2.25% (Oct 2025). Further cuts anticipated. Improving development viability and gradually expanding the homebuyer pool, but most renters remain unable to purchase.BC GDP growth projected at approximately 1.1% in 2026 — modest recovery following a weak 2025. Youth unemployment remains elevated, delaying household formation and suppressing rental demand.US–Canada tariff tensions (steel, aluminum, lumber) adding materially to construction costs and suppressing new rental starts beyond the current pipeline. Medium-term supply constraint risk from 2027 onward.Surrey offers the most affordable rental rates in Metro Vancouver at $2.59 per sq. ft. — significant value relative to Vancouver ($3.64), North Vancouver ($3.71) and Burnaby ($3.35). liv.rent Aug 2025. |

| ENVIRONMENTAL | BC Energy Step Code requirements increasing upfront construction costs on new rental developments. Heat pump mandates add cost for developers but reduce utility expenses for tenants in new stock.New 2024–2026 purpose-built units are significantly more energy-efficient than older stock, creating a growing quality and cost-of-living gap that influences tenant preferences.Flood risk in portions of South Surrey and Newton affecting insurance premiums for landlords and select development timelines for new rental projects near floodplains. |

| SOCIAL | Surrey is BC’s fastest-growing city with a population over 600,000. It is younger and more diverse than Metro Vancouver average — large South Asian, Filipino and Southeast Asian communities generate disproportionate demand for larger 2–4 bedroom units for multi-generational households.Rising renter affordability pressure is pushing households toward shared living arrangements — increasing demand for 3+ bedroom units while making the studio/1BD pipeline harder to absorb.BC Housing waitlist in Surrey is elevated. 590 supportive and affordable units proposed across three Surrey sites. Non-market supply pipeline active but insufficient relative to need.Core housing need remains acute at the bottom of the market: only 1–2% of units affordable to lower-income households were vacant in 2025. CMHC 2025. |

| TECHNOLOGICAL | Facebook Marketplace and Craigslist are the dominant platforms for private landlord listings — particularly basement suites, secondary suites, and older condo investor units. Purpose-built operators use Zumper, Rentals.ca, liv.rent, and Apartments.com.New 2024–2026 purpose-built rental buildings increasingly feature smart home technology, app-based amenity booking, keyless entry, and EV charging — commanding a premium over older stock and raising tenant expectations.City of Surrey’s digital permitting improvements (online submissions, expanded permit portal) are reducing development timelines and improving cost predictability for rental project operators. |

| LEGAL | BC Residential Tenancy Act: strong tenant protections including strict eviction rules, fixed-term lease rollover provisions, and a 3% rent increase cap for 2025. Limits landlord flexibility; most landlords not raising rents to the guideline in current market. CMHC 2025.Bill 44 (Province of BC): small-scale multi-unit zoning mandated near SkyTrain stations. Expected to unlock gentle density and increase rental supply along Surrey’s transit corridors over a 3–5 year horizon.BC Short-Term Rental Registry (Year 2, Jan 2026): enforcement returning illegally operated STRs to long-term market, adding supply and supporting tenant access.PTT exemption for purpose-built rentals (Jan 2025–Dec 2030) and CMHC’s MLI Select program are the two most impactful policy instruments currently stimulating new rental supply in Surrey. |

MARKET OUTLOOK

Near-Term: 0–12 Months (Renter’s Market)

Surrey will remain firmly in a renter’s market through 2026. Vacancy will stay elevated as the remaining purpose-built pipeline delivers. Asking rents are unlikely to increase and may decline further, particularly for studio and 1-bedroom units where absorption is weakest. Move-in incentives will persist. Tenants are well-positioned to negotiate favourable terms, particularly in newer purpose-built buildings. Basement suite and secondary suite supply will remain active on Craigslist and Facebook Marketplace at $1,000–$1,600 for 1BD.

Medium-Term: 1–3 Years (Gradual Rebalancing)

As BoC rate cuts flow through the economy, employment recovers, and delayed household formation unwinds, demand will strengthen. The slowdown in new construction starts — driven by tariffs, cost inflation, and cooling developer sentiment — will constrain the supply pipeline from 2027 onward. The market is expected to rebalance toward equilibrium (approximately 3% vacancy) by late 2027, at which point landlord pricing power will begin to return. 3BD townhouses are the unit type most likely to tighten first given the structural undersupply of family-sized rental housing relative to demand.

Structural Fundamentals (Intact)

Surrey’s long-term rental demand thesis remains strong. Population of 600,000+ growing at the fastest pace in BC. Large multi-generational household base. UBC and SFU institutional anchor. The current correction is a supply-demand timing mismatch amplified by an immigration policy shift — not a structural market failure. The undersupply of affordable family-sized rental units (2BD and larger) at the bottom of the income distribution remains acute and will not be resolved by the current pipeline.

DATA SOURCES & METHODOLOGY

Median asking prices calculated from field research comparables provided (your data, Feb 2026) — 11 listings each for 1BD and 2BD condos, 8 for 3BD condos, 11 for 3BD townhouses, 7 for 4BD townhouses. Supplemented by live Craigslist Vancouver listings (vancouver.craigslist.org/rds/apa, accessed February 26, 2026). Market data sourced from: CMHC 2025 Rental Market Report (December 12, 2025); CMHC 2025 Mid-Year Rental Market Update (July 2025); BC Government Housing Minister Statements (November 2025 and December 2025, citing Rentals.ca); Rentals.ca October 2025 National Rent Report; liv.rent August 2025 Metro Vancouver Rent Report; Zumper Rent Research (February 2026); Bank of Canada policy rate announcements. All figures are asking rents, not achieved rents. Effective rents may be lower where incentives apply. This report reflects a point-in-time snapshot of February 2026 market conditions.