January 2026 – Executive Summary

Surrey, BC | Commercial Rental Market Outlook

Market Overview by Performance Property Management

Surrey’s commercial real estate market entered 2026 in a transitional phase, characterized by

softening office fundamentals, moderating industrial conditions, and continued strength in

necessity-based retail. Elevated interest rates and slower economic growth in 2025 tempered

demand; however, population growth, infrastructure investment, and constrained land supply

continue to support long-term fundamentals across select asset classes.

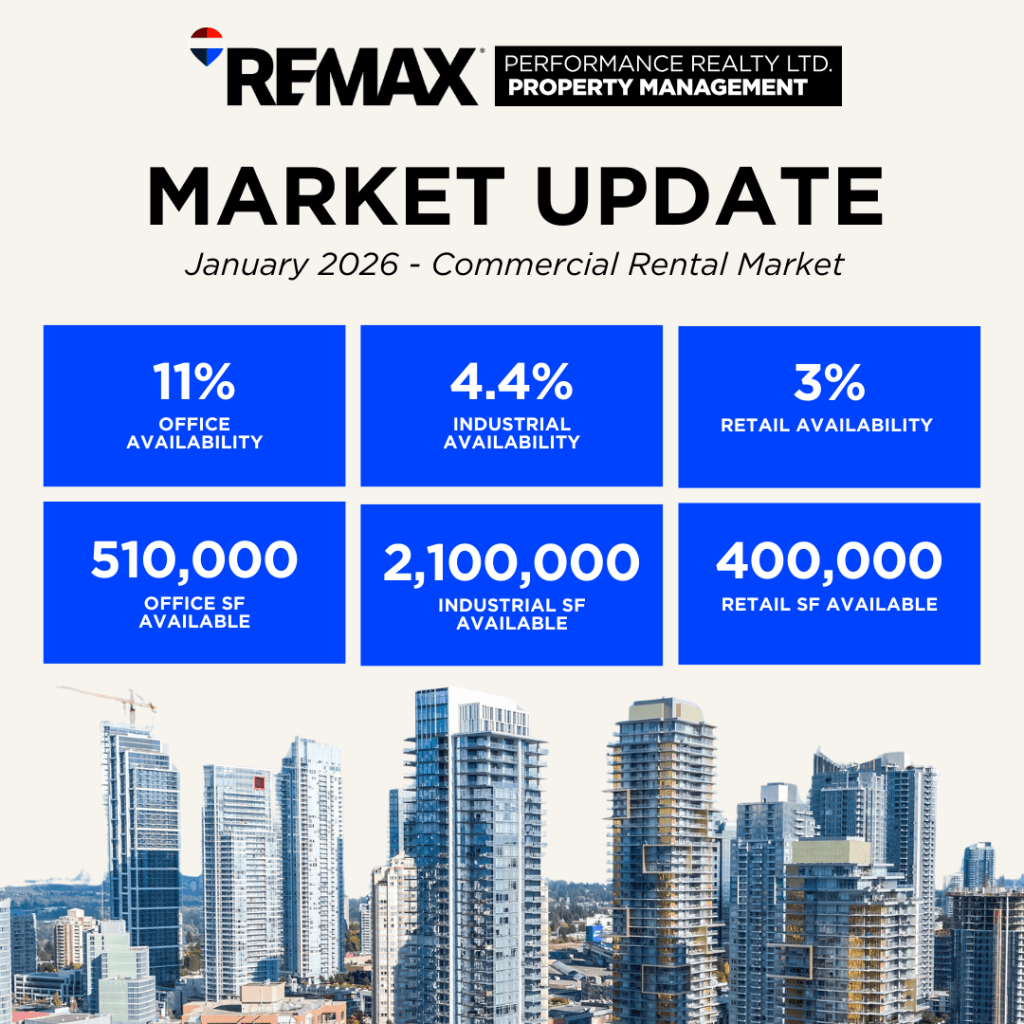

Supply & Availability Snapshot

Office:

Approximately 510,000 sq ft available (11% availability). Availability increased due to

negative net absorption and tenant downsizing.

Industrial:

Approximately 2.1 million sq ft available (4.4% availability). New supply outpaced

absorption, though fundamentals remain historically strong.

Retail:

Approximately 400,000 sq ft available (~3%). Retail availability remained tight,

supported by service-based tenant demand and limited new supply.

Demand & Leasing Velocity

Office demand remained negative at approximately –2% annually, implying a 15–18

month lease-up period.

Industrial absorption remained positive at approximately 0.6%–1.0% annually, with

lease-up periods of 5–7 months.

Retail absorption remained strong at approximately 1.5% annually, with most space

leasing within 4–6 months.

Median Rental Rates (Derived from Local brokerage listings, CoStar/Altus market data, and

recent leasing comparables)

- Office (AAA)

- Median $/Sq Ft: $35.00

- Median CAM/Sq Ft: $15.00

- Avg Sq Ft: 3,260 Sq Ft

- Office (AA-A)

- Median $/Sq Ft: $24.00

- Median CAM/Sq Ft: $14.00

- Avg Sq Ft: 2,304 Sq Ft

- Industrial

- Median $/Sq Ft: $22.00

- Median CAM/Sq Ft: $7.20

- Avg Sq Ft: 8,228 Sq Ft

- Retail

- Median $/Sq Ft: $45.00

- Median CAM/Sq Ft: $14.17

- Avg Sq Ft: 3,905

Business-Relevant Wildcards (Q4 2025–2026)

Flight to Functional Space: Businesses are prioritizing efficient, flexible, and cost-

controlled space, benefiting small-bay industrial and service retail.

Capital Discipline & Development Slowdown: Higher borrowing and construction costs

have slowed speculative development, limiting future oversupply.

Employment Growth Concentrated in Services & Logistics: Job growth in healthcare,

logistics, and personal services continues to support industrial and retail demand.

Investment Implications

Most Attractive: Small and mid-bay industrial, grocery-anchored and service retail.

Opportunistic: Select office assets with repositioning potential.

Higher Risk: Large-format commodity office assets.

Conclusion:

Industrial and necessity-based retail present the strongest risk-adjusted opportunities entering