March 2026 – Residential Rental Market Executive Summary

Surrey, BC | Condos, Townhouses & Houses Rental Market

Market Overview by Performance Property Management

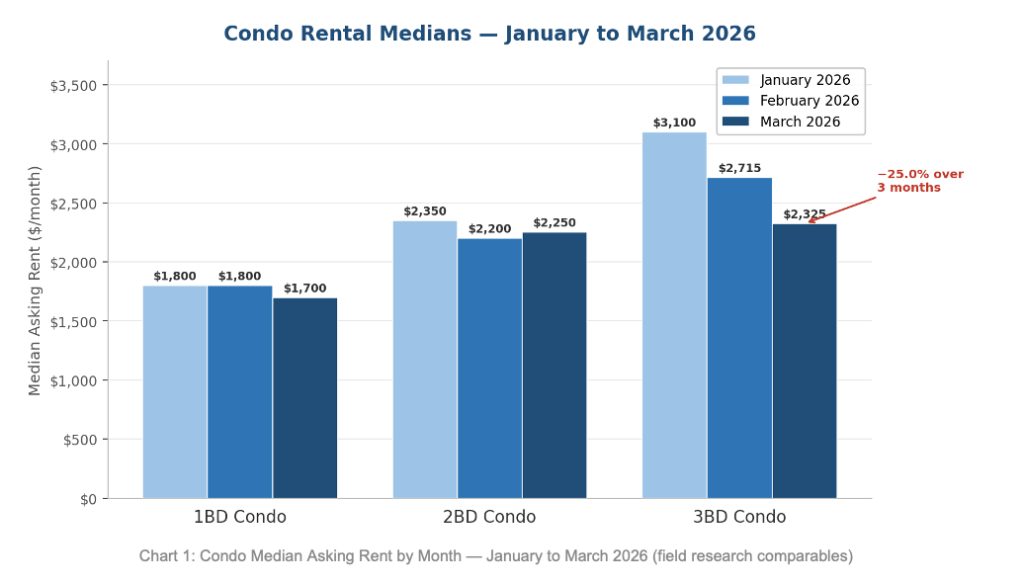

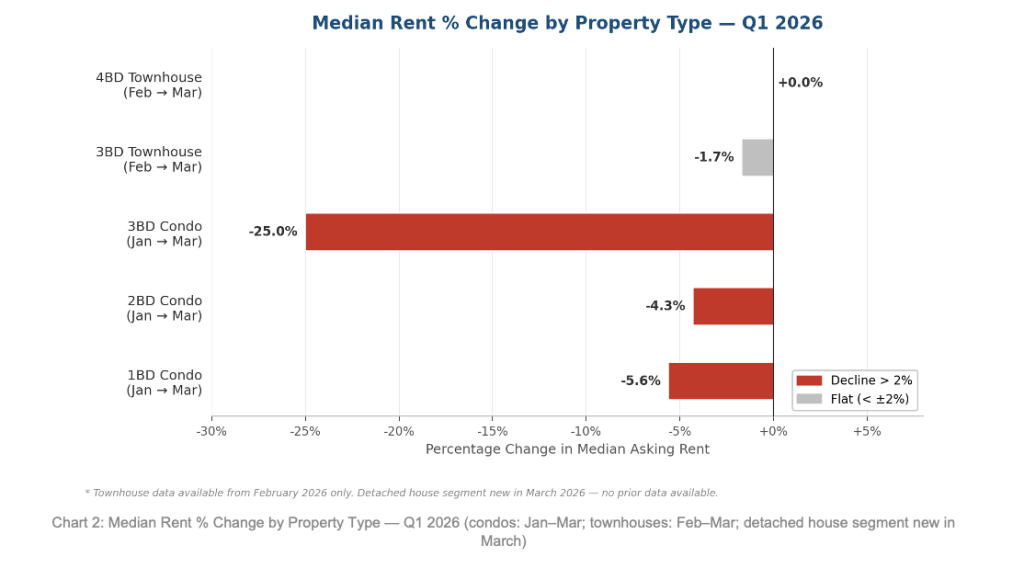

Surrey’s March 2026 delivers the sharpest single-month price movement recorded in this research series. The three-bedroom condo segment — which held firm through most of 2025 — has broken lower, with the median falling $390 in one month to $2,325, a 14.4% decline from February’s $2,715. The one-bedroom median also softened further, down $100 to $1,700. The two-bedroom segment bucked the trend, edging up $50 to $2,250 — evidence of diverging absorption dynamics: smaller and larger condo formats are accumulating on the market while mid- sized, two-bedroom units are being absorbed. Townhouses showed notable resilience — the 3BD median slipped just $50 to $2,850 and 4BD held flat at $3,200, reinforcing the view that family-format rentals remain the scarcest and most durable product in Surrey’s rental stack.

This month’s dataset expands for the first time to include detached houses (11 comparables). Houses are commanding a median of $3,800/mo across a wide range of $3,200–$4,200, with average days on market of 30 — the longest absorption time of any tracked segment. A standard deviation of $276 reflects a market still price-discovering, with significant variance driven by bedroom count, square footage, and location. Larger homes in Newton and Fleetwood ($4,000–$4,200) sit alongside more compact, mid century stock in Cloverdale and Guildford ($3,200–$3,600).

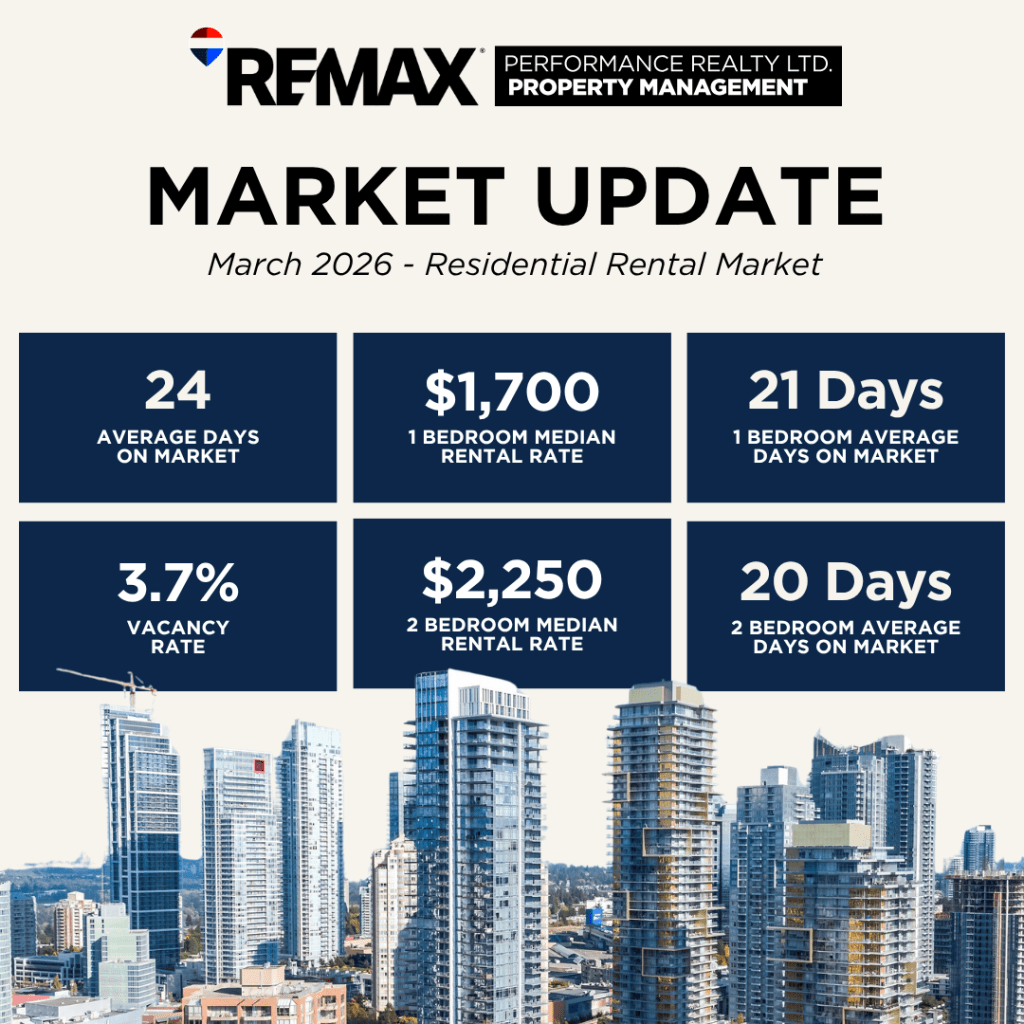

The macro backdrop remains firmly in tenants’ favour. Greater Vancouver’s vacancy rate holds at 3.7% — the highest since the early 1990s — and Surrey’s studio and one-bedroom units continue to face the region’s most difficult absorption conditions. Move-in incentives are still active across the market. Structural demand, anchored by 600,000+ residents and a young, growing population, is intact — but continues to be outpaced by a pipeline of smaller-format purpose-built supply that the market cannot yet absorb at the pace of delivery.

Key findings from March 2026 field research (11 listings each for 1BD/2BD/House, 8 for 3BD condo, 11 for 3BD TH, 7 for 4BD TH):

Detached houses (new segment): median $3,800, range $3,200–$4,200, average DOM 30 days. Size (1,550–2,800 sq. ft.) is the dominant pricing variable.

1BD condo: median $1,700, down 5.6% MoM. Tight price band ($1,600–$1,895) almost entirely explained by build year and amenity package. Average DOM steady at 21 days — well-priced units still leasing within three weeks.

2BD condo: median $2,250, the only segment to post a month-over-month gain (+$50). Listings clustered between $2,150 and $2,350; a 900 sq. ft. 1999-vintage unit on 104 Ave & 150 St anchored the low end.

3BD condo: median $2,325, the month’s headline move, down $390 (14.4%). Two 2026-vintage units near King George Blvd listed at $2,000, pulling the floor sharply lower. 1990s Guildford stock (10736 & 10463 150 St) priced $2,200–$2,400 despite offering 1,039–1,200 sq. ft., reflecting the market’s deep discounting of older product regardless of size.

3BD townhouse: median $2,850, essentially flat MoM. Range held tight at $2,500–$3,000 with average DOM of 20 days — the fastest-clearing segment in the dataset.

4BD townhouse: median $3,200, unchanged. Average DOM widened slightly to 27 days; one Cloverdale listing sat 50 days, the longest tenure in the townhouse sample.

MEDIAN ASKING PRICES

March 2026 field research spans 59 comparables across six segments — the most comprehensive dataset in this series, expanded this month by the addition of 11 detached house listings. All figures are asking rents. Where move-in incentives apply (confirmed active across multiple Surrey listings in March 2026), effective rents are typically 8–17% lower on an annualized basis for a one-month-free arrangement.

The data this month tells a split-market story across the condo stack. The 1BD decline is a persistent, grinding attrition driven by oversupply of small-format units competing with a thin pool of single-occupant renters. The 3BD condo drop is a different and more significant signal: new 2026-vintage units entering the market at $2,000 are resetting price expectations for an entire segment, with the Guildford vintage stock now facing the uncomfortable reality of competing on price — not just age — against brand-new product. Meanwhile, the two-bedroom format is demonstrating genuine resilience, likely because it serves the broadest demand base: couples, small families, and shared households alike. Townhouses and houses continue to occupy a supply-constrained tier where family demand remains firm.

| UNIT TYPE | MEDIAN/MO. | MINIMUM | MAXIMUM | AVERAGE DOM |

| 1 Bed / 1 Bath – Condo | $1,700 | $1,600 | $1,895 | 21 days |

| 2 Bed / 1–2 Bath – Condo | $2,250 | $1,900 | $1,895 | 20 days |

| 3 Bed / 1+ Bath – Condo | $2,325 | $2,000 | $2,550 | 25 days |

| 3 Bed / 2+ Bath – Townhouse | $2,850 | $2,500 | $3,000 | 20 days |

| 4 Bed / 2+ Bath – Townhouse | $3,200 | $2,950 | $3,300 | 27 days |

| 4+ Bed / 2+ Bath – House | $3,800 | $3,200 | $4,200 | 30 days |

Key Observations

- Build year is now the most powerful pricing variable in the condo market. The 1BD spread from $1,600 (2018 stock at 13573 98A Ave) to $1,895 (2025 build at 104 Ave & Whalley) is a $295 gap driven almost entirely by vintage, not location. The same dynamic plays out more dramatically in 3BD condos, where the 1990s Guildford stock lists at $2,200–$2,400 while 2024–2026 equivalents command $2,500–$2,550.

- The 3BD condo segment has repriced materially this month. Two 2026-vintage units near King George Blvd asked $2,000 — a full $550 below the segment median in February. Landlords of 2010s-era product now face downward pressure from both ends: older 1990s stock competing on square footage and newer 2026 stock competing on price.

- The two-bedroom condo is March’s relative bright spot. With listings clustered tightly at $2,150–$2,350 and an average DOM of just 20 days, this format is clearing faster and more consistently than any condo category. The 104 Ave & 140 St unit (2022 build, $2,250, 700 sq. ft.) sat 40 days — the only real outlier, likely reflecting a pricing or presentation misstep rather than segment weakness.

- Townhouses are the market’s most stable segment by every measure. The 3BD TH range of $2,500–$3,000 is the tightest of any category, average DOM is 20 days, and the segment has moved just $50 in two months. This consistency reflects structural undersupply of family-format rentals relative to demand in Surrey’s multi-generational household base.

- Detached houses are price-discovering. The $3,200–$4,200 range is the widest recorded this month, and a standard deviation of $276 is more than double that of any condo segment. Square footage (1,550–2,800 sq. ft.) is the dominant driver; location plays a secondary role. At 30 days average DOM, houses take longer to lease than townhouses despite commanding a premium — suggesting tenants evaluate detached rentals with more deliberation and fewer urgent movers.

- The DOM signal is becoming more differentiated across segments. Three-bedroom condos averaged 24.5 days — the longest of any condo format and up from 24 days in February — as the supply wave of larger investor-owned condos accumulates. One-bedroom condos averaged 21 days despite being the most oversupplied type, which reflects the large pool of single-renter demand still present in Surrey’s City Centre corridor.

Q1 2026 Rent Trend Analysis

The two charts below visualise median asking rent movements across all tracked property types from January through March 2026. Chart 1 shows absolute median rents by condo segment month-over-month. Chart 2 summarises percentage change over the full Q1 period for condos (January–March) and February–March for townhouses, where January data was not available.

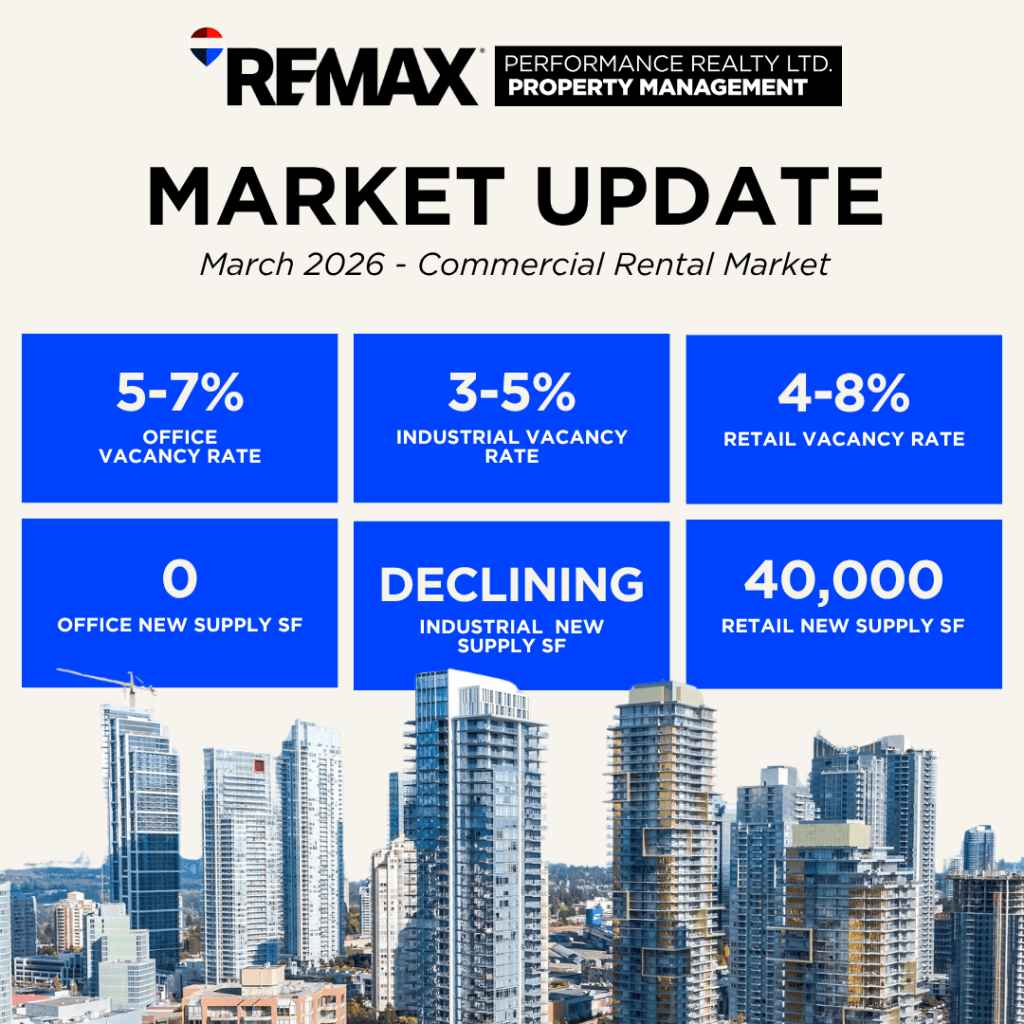

2. SUPPLY

The supply picture in March 2026 is entering a new phase. The initial wave of purpose-built rental completions that drove vacancy to 3.7% is largely delivered; what the market is now absorbing is the tail of that pipeline. The more significant supply story is compositional: the units that arrived were disproportionately studio and one- bedroom, and the market data confirms they are the hardest to place. The entry of new 2026-vintage three-bedroom condos at $2,000 in March — below the segment median by $325 — suggests that even larger new-build units are being priced aggressively to secure occupancy, which is a new dynamic not observed in 2025. Developer confidence is softening on net-new starts, and the tariff environment is adding real cost uncertainty to any project not already under construction. The current oversupply is transitional, but the transition period is proving longer than initially anticipated.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Metro Vancouver rental completions (2025) | Above 5-yr average | CMHC 2025 Rental Market Report – concentrated in City of Vancouver but strong in Surrey |

| National purpose-built vacancy rate | 3.1% (Oct 2025) | Up from 2.2% (Oct 2024); CMHC 2025 Rental Market Report |

| Greater Vancouver vacancy rate | 3.7% (Oct 2025) | Highest in 30+ years – more than doubled from 1.6% in 2024 |

| Surrey: new stock leasing difficulty | Elevated | CMHC 2025: studio/1BD mix less desirable; heavy competition from condo completions |

| Rental unit mix mismatch | Studio/1BD heavy | Pipeline skewed to smaller units; demand stronger for 2–3BD family-sized units |

| Move-in incentives | 1–2 months free rent | Active across Surrey – confirmed Craigslist Mar 2026 & CMHC 2025 annual report |

| Short-term rental returns | Units returning to LTR | BC STR registry Year 2 (Jan 2026): thousands of units added to long-term supply |

3. DEMAND

Demand in March 2026 is showing its first internal differentiation. The broad softening of 2025 — driven by reduced immigration, elevated youth unemployment, and suppressed household formation — is still the dominant force. But within that softness, the two-bedroom condo’s ability to tick up $50 while the one-bedroom and three- bedroom formats declined points to a shrinking renter pool. Shared households and small families are actively competing for two-bedroom product, keeping that segment firm. Solo renters and students — the primary demand base for one-bedroom units — are either doubling up, staying home, or holding out for better deals. Three- bedroom renters face an unusual situation: new supply entering at prices below existing comparable stock, which means the patient tenant can now wait for a better unit at a lower price. Surrey’s structural demand attributes — population above 600,000, the youngest and fastest-growing base in Metro Vancouver, institutional anchors at SFU Surrey and the planned UBC campus, and a multi-generational household culture driving disproportionate demand for 3+ bedroom formats — remain fully intact. The current weakness is a cyclical overlay on a fundamentally sound demand base.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Surrey Population | 600,000+ (BC’s fastest growing) | City of Surrey 2025. Structural long-term demand base |

| Immigration targets reduced | Federal cuts 2025-2027 | Non-permanent resident outflow in BC; most NPRs are renters. CMHC 2025 |

| International Students | Declining | Federal study permit cap (2024–2025). SFU Surrey & planned UBC campus support local demand |

| Youth Unemployment | Elevated | Slow wage growth reducing household formation. CMHC 2025 |

| Surrey 1BD asking rent change | −3.6% YoY (Mar 2026 est.) | Continued decline from −9.3% YoY (Dec 2025); pace of decline moderating |

| Surrey all-type median | $1,950/mo (Feb 2026) | Zumper Rent Research Feb 2026 – down ~11% in last year |

| Tenant negotiating power | Strongest in a decade | Vacancy above 3.7%, incentives widespread; clearest renter’s market since 1990s |

| Affordable units vacancy | Still very tight (1–2%) | Only 1–2% of units affordable to lower-income households were vacant. CMHC 2025 |

3. FUEL

The capital environment in March 2026 is characterized by a widening divergence between conditions for tenants and conditions for developers. For tenants, the Bank of Canada’s rate reductions have improved mortgage affordability at the margin — but ownership remains out of reach for the majority of Surrey renters, and the primary effect of lower rates in the rental market has been to reduce the carrying costs of investor-owned condo landlords rather than to convert tenants into buyers. For developers, the picture is more challenging: US–Canada tariffs on steel, aluminum, and lumber are adding a measured but real cost burden to any project breaking ground now, and the softening of condo presales — a leading indicator of future secondary rental supply — is beginning to thin the pipeline for 2028–2030 delivery. The policy levers are working in the right direction. The BC Property Transfer Tax exemption for purpose-built rentals (active through December 2030) and CMHC’s MLI Select program are the two most impactful instruments, and both are actively deployed in Surrey. City of Surrey’s permitting acceleration — 75% faster processing in 2025 — is compressing the carrying cost window for new projects. However, these incentives are offsetting rather than overcoming the cost headwinds; net-new starts remain below the pace needed to sustain supply into 2028.

| METRIC | VALUE / RANGE | SOURCE & NOTES |

| Bank of Canada policy rate | 2.25% (Oct 2025) | Further cuts anticipated into 2026; improving landlord carry costs |

| Impact on renters | Mixed | Lower rates improve homebuying affordability marginally; most renters still locked out |

| BC Property Transfer Tax exemption | In effect Jan 2025–Dec 2030 | Purpose-built rental buildings exempt from PTT; stimulating supply-side activity |

| Federal Rental Construction Financing | Active (RCFi / MLI Select) | CMHC low-interest loans for rental construction; active in Surrey |

| Construction cost environment | Constrained | US–Canada tariffs on steel, aluminum, lumber adding 5–15% to costs. CMHC Fall 2025 |

| Developer confidence | Softening for new starts | Condo presales declined significantly – leading indicator of future supply tightening |

| BC Rent Increase Guideline | 3.0% cap (2025) | Most same-sample increases below guideline – landlords not exercising full rights |

| City of Surrey permitting | 75% faster (2025) | $35.1M invested in housing; 20+ process improvements reducing carrying costs |

PEESTEL FACTORS

The following Political, Economic, Environmental, Social, Technological and Legal factors are shaping the Surrey residential rental market as of March 2026. Several factors have evolved since February: the tariff environment has hardened as a near-term construction cost risk, the BC government’s housing policy posture is increasingly focused on demonstrating progress ahead of electoral cycles, and the first 2026-vintage rentals entering the market at below-market pricing are creating a new data point for policy observers and developers alike.

| POLITICAL | Federal election year: housing affordability a top-tier campaign issue. Reduced immigration targets (2025–2027) are the single largest near-term driver of demand softening. BC Provincial government citing rising vacancy rates as a policy success. Short-term rental registry (Year 2, Jan 2026) returning units to long-term rental market. City of Surrey approved $35.1M in housing investments in 2025. OCP update underway to support densification. Bill 44 upzoning near SkyTrain stations. |

| ECONOMIC | Bank of Canada policy rate at 2.25% (Oct 2025); further cuts anticipated. BC GDP growth projected at ~1.1% in 2026. Youth unemployment remains elevated, delaying household formation. US–Canada tariff tensions adding materially to construction costs, suppressing new rental starts beyond current pipeline. Surrey remains most affordable in Metro Vancouver at $2.59/sq. ft. vs Vancouver ($3.64) and North Vancouver ($3.71). liv.rent Aug 2025. |

| ENVIRONMENTAL | BC Energy Step Code requirements increasing upfront construction costs. Heat pump mandates add cost for developers but reduce utility expenses for tenants. New 2024–2026 purpose-built units significantly more energy-efficient than older stock. Flood risk in portions of South Surrey and Newton affecting insurance premiums for landlords. |

| SOCIAL | Surrey is BC’s fastest-growing city (600,000+). Younger and more diverse than Metro Vancouver average; large South Asian, Filipino, and Southeast Asian communities generate disproportionate demand for 2–4 bedroom units. Rising affordability pressure pushing households toward shared living, increasing demand for 3+ bedroom units. BC Housing waitlist in Surrey elevated; 590 supportive and affordable units proposed. Non-market supply pipeline active but insufficient. |

| TECHNOLOGICAL | Facebook Marketplace and Craigslist dominate for private landlord listings – especially basement suites and older condo investor units. Purpose-built operators use Zumper, Rentals.ca, liv.rent, and Apartments.com. New 2024–2026 purpose-built rental buildings increasingly feature smart home technology, app-based amenity booking, keyless entry, and EV charging. City of Surrey’s digital permitting improvements reducing development timelines. |

| LEGAL | BC Residential Tenancy Act: strict eviction rules, fixed-term lease rollover provisions, and 3% rent increase cap for 2025. Bill 44: small-scale multi-unit zoning mandated near SkyTrain stations; expected to unlock gentle density along Surrey’s transit corridors over 3–5 years. BC Short-Term Rental Registry (Year 2, Jan 2026): enforcement returning illegally operated STRs to long-term market. PTT exemption for purpose-built rentals (Jan 2025–Dec 2030) and CMHC MLI Select are the two most impactful policy instruments currently stimulating new rental supply. |

MARKET OUTLOOK

Near-Term: 0–12 Months (Renter’s Market Deepening)

The March data introduces a new concern for landlords: price competition between new-build and legacy stock within the same segment. The 3BD condo market is now experiencing exactly this — 2026-vintage units at $2,000 competing against 2020–2024 units at $2,250–$2,550 competing against 1990s stock at $2,200–$2,400. This three-way compression will continue to erode median prices until the new-build pipeline clears. Landlords of older stock face the least favourable position: they cannot compete on amenity, they cannot easily drop below debt service, and they are now also competing against peers pricing aggressively to achieve occupancy. Move-in incentives will remain standard. The one-bedroom market’s 21-day average DOM, while serviceable, is being

maintained through pricing discipline — landlords who resist further reductions will see that figure extend quickly.

Medium-Term: 1–3 Years (Rebalancing on a New Floor)

The medium-term outlook is rebalancing, but toward a structurally lower rent floor than the market anticipated twelve months ago. The combination of 2026-vintage units entering below previous price expectations, slowing net-new starts, and a gradual demand recovery as immigration policy stabilises and household formation resumes will bring vacancy back toward 3% by 2027–2028. The question is what equilibrium rents look like at that vacancy level. Given the reset in 3BD condo pricing and the persistence of 1BD softness, the rebound from current levels is likely to be modest — recovery to late-2024 rents, not to 2022–2023 peaks. Townhouses and detached houses are the exception: supply constraints in these formats are structural, and once demand recovers, 3BD TH is positioned to tighten first and fastest.

Structural Fundamentals (Intact, but Patience Required)

Surrey’s long-term rental demand thesis is unchanged and remains among the strongest in Canada. A population exceeding 600,000, the fastest growth rate in BC, a young and diverse demographic profile, and institutional demand anchors at SFU Surrey and the incoming UBC campus all point to durable rental need. The current period of oversupply and falling rents is a supply-demand timing mismatch — amplified by a federal immigration reset — not evidence of structural market failure. The most acute unmet need remains at the affordable end: only 1–2% of units accessible to lower-income households were vacant in 2025, a gap the current pipeline will not close. Investors and operators with a three-to-five year horizon are acquiring into a market that has likely found its floor.

DATA SOURCES & METHODOLOGY

Median asking prices calculated from field research comparables provided (Mar 2026) — 11 listings each for 1BD and 2BD condos, 8 for 3BD condos, 11 for 3BD townhouses, 7 for 4BD townhouses, and 11 for detached houses. Supplemented by live Craigslist Vancouver listings (vancouver.craigslist.org/rds/apa, accessed March 2026). Market data sourced from: CMHC 2025 Rental Market Report (December 12, 2025); CMHC 2025 Mid-Year Rental Market Update (July 2025); BC Government Housing Minister Statements (November 2025 and December 2025, citing Rentals.ca); Rentals.ca October 2025 National Rent Report; liv.rent August 2025 Metro Vancouver Rent Report; Zumper Rent Research (February 2026); Bank of Canada policy rate announcements. All figures are asking rents, not achieved rents. Effective rents may be lower where incentives apply. This report reflects a point-in-time snapshot of March 2026 market conditions.