March 2026 – Executive Summary

Surrey, BC | Commercial Rental Market Outlook

Market Overview by Performance Property Management

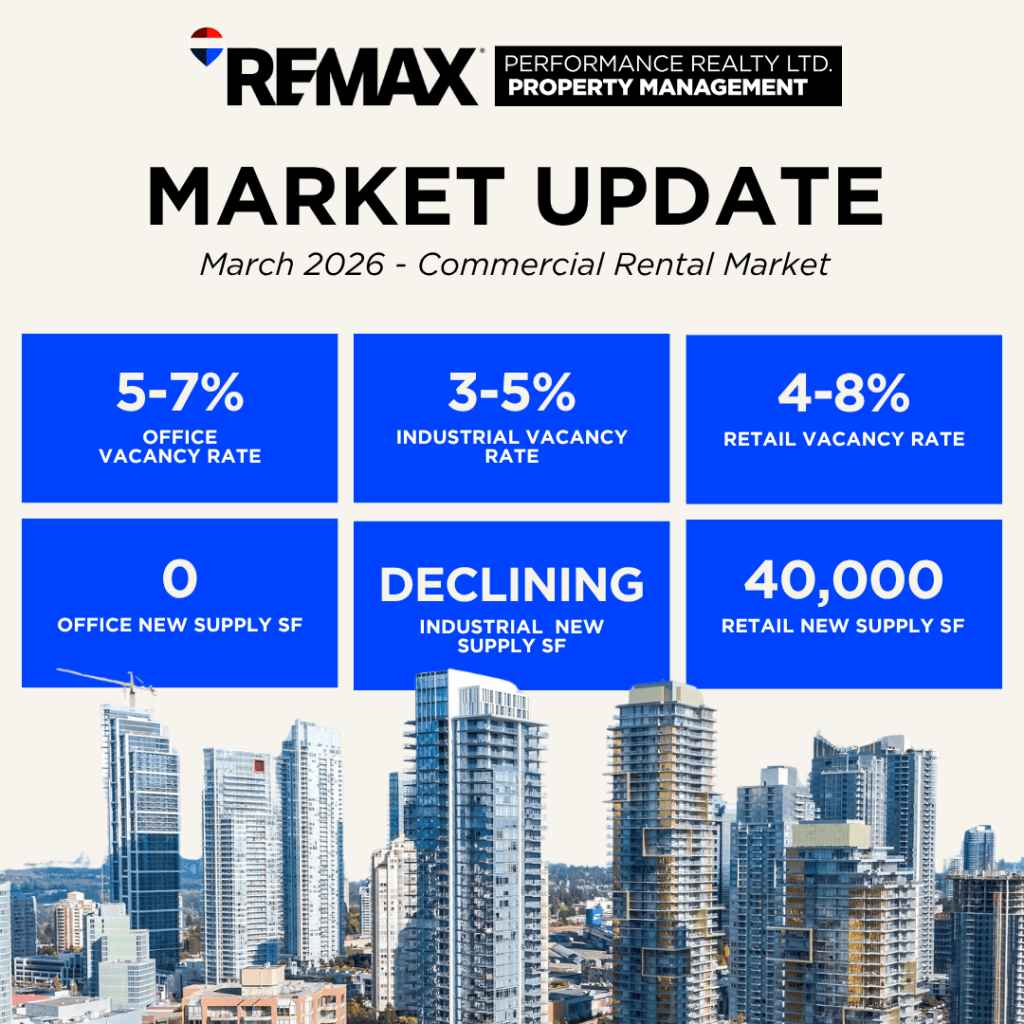

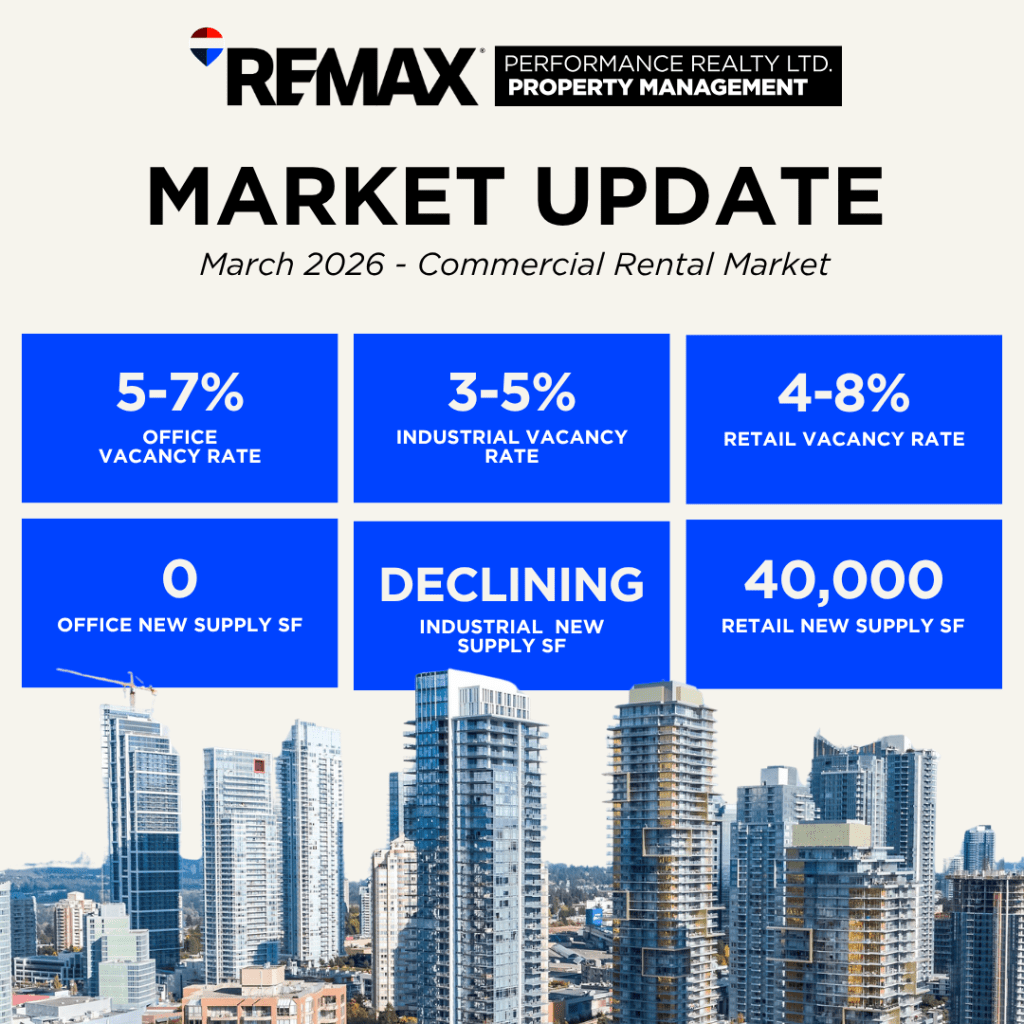

Surrey’s commercial leasing market enters March 2026 navigating a more complex external environment than in February, shaped by three dominant forces: the escalating US-Canada trade conflict, a new BC Budget expanding PST to commercial real estate services, and the imminent CUSMA renegotiation (July 1, 2026). Against this backdrop, the underlying fundamentals of each asset class have shifted modestly but not dramatically since the February 2026 report.

Office demand is strengthening on the back of gross leasing activity that doubled across Metro Vancouver in 2025, though vacancy remains sticky at approximately 12.4% across suburban markets. Industrial vacancy is approaching a probable peak regionally, with large-format absorption surging in Q4 2025 and CBRE projecting that large-format supply could be cut in half by mid-2026. Retail is fundamentally healthy outside regional malls, with the HBC anchor void at Central City and the City Centre 4 retail podium lease-up the two defining watch items for Surrey in 2026.

| 100% Metro Van Gross Leasing | ~4.8% Metro Van Industrial Vacancy Peak | 2–4% Non-Mall Retail Vacancy | Oct 2026 BC PST Expands to CRE Services |

OFFICE MARKET

Metro Vancouver’s office market entered 2026 with genuine momentum: gross leasing activity doubled in 2025 versus 2024, and 72% of Avison Young professionals surveyed expect leasing activity to outperform in 2026 (Avison Young Q4 2025). However, vacancy remains ‘sticky’ at approximately 12.4% across the region — a function of large blocks of space being returned to the market simultaneously as new deals are signed, TI allowances that have risen 125% since 2019 ($77.49 psf on average), and the ongoing challenge of leasing Class B/C space under 5,000 sf. No new office supply is expected in Metro Vancouver beyond projects already paused. Surrey City Centre is well-positioned relative to peers.

Class AAA — Health & Technology District

City Centre 4 is now fully delivered and operational, cementing the Health & Technology District’s position as Surrey’s premier office precinct and the most significant suburban medical-tech cluster in BC. The precinct now totals over 500,000 sf of AAA office and retail space. Lease-up activity is ongoing but no public asking rate has been confirmed.

| METRIC | VALUE | NOTES & SOURCES |

| Total Inventory | ~500,000 sf | Health & Technology District — City Centre 4 (CC4) fully delivered; precinct now totals over ½M sf of AAA office and retail (LoopNet, Mar 2026) |

| New Supply | Nil (Q1 2026) | CC4 fully delivered in Q4 2025. No AAA groundbreakings active; all planned Metro Vancouver office projects paused (CBRE Vancouver 2026 Outlook, Jan 2026) |

| Vacancy Rate | ~5–7% | Unchanged from Feb 2026. CC4 lease-up ongoing. No independent Surrey AAA vacancy data published — triangulated from Metro Vancouver suburban figures |

| Net Asking Rate | $40–$48 psf/yr | No public listed rate; broker-estimated from regional AAA benchmarks. Verify directly with Nicola Institutional Realty Advisors (LoopNet listing active Mar 2026) |

| Additional Rent | $18–$22 psf/yr | LEED Gold operating cost estimate; consistent with Metro Vancouver trophy suburban norms |

| Total Rent | $58–$70 psf/yr | Net + Additional — all-in occupancy cost estimate |

| Demand Profile | Health · Tech · Academic · Gov’t | Surrey Memorial Hospital adjacency; SFU Surrey; planned UBC campus; medtech and digital health cluster expanding |

Class AA — City Centre Premium

Class AA City Centre assets, led by Central City Tower (BOMA BEST Gold), are benefiting from the

broader return-to-office trend and flight-to-quality demand. With no new supply entering the market, any incremental demand recovery will compress vacancy directly. Large-block availability (30,000+ sf) across Metro Vancouver rose 20% in 2025 as companies right-sized, but this is a Metro-wide trend — Surrey City Centre’s smaller-format, transit-accessible product faces less of this pressure.

| METRIC | VALUE | NOTES & SOURCES |

| Total Inventory | ~1.2–1.5M sf (est.) | City Centre towers and premium suburban; Central City Tower (25-storey, BOMA BEST Gold) is the benchmark AA asset |

| New Supply | Nil (Q1 2026) | No new AA deliveries in 2026; all speculative office development paused region wide (CBRE Jan 2026; Avison Young Q4 2025) |

| Vacancy Rate | ~8–11% | Metro Vancouver suburban Class A vacancy ~12.4% overall (Avison Young Q4 2025); Surrey City Centre outperforming at estimated 8–11% given 2025 absorption |

| Net Asking Rate | $32–$40 psf/yr | LoopNet live listings: Central City (Nicola Institutional, contact-broker); Commercial Search range $20–$30 psf for suburban Surrey |

| Additional Rent | $16–$20 psf/yr | Standard Metro Vancouver suburban OpEx; BOMA certified buildings carry higher TMI |

| Total Rent | $48–$60 psf/yr | Competitive vs Downtown Vancouver all- in $50–$65+ psf; RTO mandates supporting demand (Avison Young Q4 2025) |

| Demand Profile | Professional services · Finance · Gov’t | Gross leasing up 100% in Metro Vancouver in 2025 vs 2024 (CBRE Jan 2026); flight to-quality still dominant; large-block 30K+ sf availability up 20% (space being returned) |

Class A — Suburban Business Parks

Class A suburban parks remain the most challenged office tier in Surrey. The proliferation of

available options — over 900 choices under 5,000 sf across Metro Vancouver — gives tenants

maximum leverage. Landlords are responding with rising TI packages (Metro Van. avg $77.49 psf,

Avison Young Q4 2025) to differentiate. Older product without transit access or modern fit-out is

taking significantly longer to lease. Tariff-related business uncertainty is causing SME tenants to

defer relocation decisions.

| METRIC | VALUE | NOTES & SOURCES |

| Total Inventory | ~3–4M sf (est.) | Newton, Cloverdale, 96 Ave business parks, South Surrey; estimated from municipal data |

| New Supply | Nil (Q1 2026) | No speculative Class A suburban groundbreakings; Class B/C small-format (<5,000 sf) under greatest pressure (CBRE Jan 2026) |

| Vacancy Rate | ~10–14% | Class B/C <5,000 sf struggling most to lease (CBRE). Sublease now 18% of Metro Van. vacancy vs 40% in 2021 — fewer turnkey options for tenants |

| Net Asking Rate | $18.64–$36 psf/yr | Live LoopNet listings (Mar 2026): Highland Business Centre (Campbell Heights) $18.64 psf · 9180 King George Blvd $24.00 psf · 9288 120 St (Scott Rd) $36.00 psf |

| Additional Rent | $12–$16 psf/yr | Lower OpEx than City Centre; ample surface parking typical in suburban parks |

| Total Rent | $34–$48 psf/yr | Value positioning vs Burnaby/Richmond Class A ($45–$55+ gross) |

| Demand Profile | Medical · Professional services · Back-office | TI allowances rising — Metro Van. avg $77.49 psf (up 125% since 2019, Avison Young Q4 2025). Smaller tenants seeking turnkey space; 900+ options sub-5K sf |

INDUSTRIAL MARKET

Surrey’s industrial market is approaching a significant inflection point. National industrial vacancy plateaued at 5.2% in Q4 2025, potentially signalling the end of the correction cycle (JLL, Feb 2026). Locally, large-format demand has surged strongly in H2 2025, with CBRE projecting that Metro Vancouver’s large-format industrial supply could be cut in half by mid-2026 as absorption outpaces new completions. The construction pipeline is contracting meaningfully, with Cushman & Wakefield forecasting vacancy to peak at approximately 4.8% before easing to 4.5% by 2027.

The primary new risk factor since the February report is the escalating tariff environment. Building material tariffs — steel at 50%, aluminum at 50%, lumber at 10%+ — are compressing developer margins and suppressing new starts. This paradoxically supports medium-term rent recovery as the pipeline shrinks, while creating near-term occupier hesitation among trade exposed tenants. Surrey’s position as a gateway to the Pacific Highway border crossing and US market is both a structural advantage and a tariff-exposure risk, depending on tenant type.

| METRIC | VALUE | NOTES & SOURCES |

| ── LARGE FORMAT LOGISTICS (100,000+ sf) | ||

| Total Inventory | ~25M sf (Metro Van.) | Surrey nodes: Campbell Heights · Port Kells · Colebrook · South Campbell Heights (expansion approved Dec 2024) |

| New Supply | Declining | Pipeline contracting; new industrial starts slowing (C&W Jun 2025); vacancy expected to peak ~4.8% then ease to 4.5% by 2027 |

| Vacancy Rate | ~3.0–4.8% (Metro Van.) | C&W Jun 2025: Metro Van. vacancy approaching 4.8% peak. Surrey below average. JLL Feb 2026: national industrial vacancy plateaued Q4 2025 at 5.2% |

| Net Asking Rate | $19–$22 psf/yr | Live LoopNet (Mar 2026): 15030 54A Ave (CBRE) $19.00 psf · Cedar Coast South Surrey $18.00 psf. Rents to remain below $20 psf Jun 2025–Dec 2027 (C&W) |

| Additional Rent | $6–$8 psf/yr | Standard Metro Vancouver industrial TMI; consistent with all prior periods |

| Total Rent | $25–$30 psf/yr | Down from $31+ peak in 2022; tariff uncertainty causing occupier hesitation on space commitments |

| Demand Profile | 3PL · Distribution · E-commerce | Large-format demand surging in H2 2025 — CBRE Jan 2026: large-format supply could be cut in half by mid 2026. Strong positive absorption in Q4 2025 |

| ── MID-BAY (20,000–100,000 sf) | ||

| Total Inventory | Significant (est.) | Newton · Port Kells · Cloverdale; no standalone Surrey mid-bay inventory count published |

| New Supply | Moderate | Some mid-bay delivered in speculative cycle; starts now slowing |

| Vacancy Rate | ~3–5% | Slightly elevated vs large format; tariff uncertainty slowing SME expansion decisions |

| Net Asking Rate | $17–$20 psf/yr | Live LoopNet (Mar 2026): Building A — 13018 80 Ave (Lee & Assoc.) $19.50 psf · 9295 198th St (Lee & Assoc.) $19.00–$19.50 psf |

| Additional Rent | $6–$8 psf/yr | Consistent with all Surrey/Langley product |

| Total Rent | $23–$28 psf/yr | Landlords offering free rent and flexible terms; moderate inducements available |

| Demand Profile | Light manufacturing · Warehousing · Distribution | Trade uncertainty creating ‘wait-and-see’ stance; nearshoring potential longer-term upside for BC (NAIOP 2025) |

| ── SMALL BAY (<20,000 sf) | ||

| Total Inventory | Widespread | Distributed across all Surrey nodes; strata and leasehold product |

| New Supply | Limited | New small-bay strata constrained by land costs and construction cost inflation (tariffs on steel/aluminum/lumber) |

| Vacancy Rate | ~5–7% | Softest segment; SME caution most acute — tariff uncertainty particularly impacts trade-exposed small businesses |

| Net Asking Rate | $14–$19.95 psf/yr | Live LoopNet (Mar 2026): 13365 115th Ave flex $19.95 psf · Cambridge Business Centre $25.00 psf · 19135 94th Ave (Port Kells) $15.95 psf |

| Additional Rent | $5–$7 psf/yr | Lower TMI than larger formats; older building stock |

| Total Rent | $19–$25 psf/yr | Landlord flexibility required; longer lease- up periods vs prior cycle |

| Demand Profile | SME · Trades · Service businesses | Most exposed to tariff uncertainty and credit tightening; recovery tied to BoC cuts flowing through to SME sector |

RETAIL MARKET

Surrey’s retail market fundamentals remain sound across non-mall formats, with strip and neighbourhood vacancy stable at 2–4% (CBRE Jan 2026). The BC consumer has proved more resilient than anticipated, outspending provincial counterparts per capita across major spending categories. However, March 2026 brings new risks to the retail outlook: tariff-driven consumer caution on discretionary goods, uncertainty around the CUSMA review, and the imminent delivery of City Centre 4’s 40,000 sf retail podium — one of Metro Vancouver’s most watched supply events of 2026.

The HBC anchor void at Central City Mall remains unresolved and continues to represent the single largest risk in Surrey retail. CBRE is actively watching what happens with HBC space regionally. BMO’s March 2026 commercial outlook notes that retailers focused on everyday essentials and services are likely to outperform those offering discretionary products made more expensive by tariffs; strip malls anchored by grocers are expected to outperform indoor malls.

| METRIC | VALUE | NOTES & SOURCES |

| ── CITY CENTRE / MIXED-USE PODIUM | ||

| Total Inventory | ~1.5M sf (est.) | City Centre core, Central City, City Centre 4 retail podium — 40,000 sf new supply delivering 2026 (CBRE Jan 2026) |

| New Supply | ~40,000 sf (2026) | City Centre 4 (CC4) retail podium — one of Metro Van.’s key retail supply events for 2026; CBRE watching pre leasing activity and rental rates closely |

| Vacancy Rate | ~4–8% | HBC anchor void at Central City unresolved — largest single vacancy risk in Surrey retail. CC4 podium lease-up to be monitored closely in Q2–Q3 2026 |

| Net Asking Rate | $28–$42 psf/yr | No public CAD listed rates for CC4 podium. Estimated from LoopNet.com USD listings and CBRE H1 2025 Retail Rent Survey (converted ~1.38 USD/CAD) |

| Additional Rent | $14–$18 psf/yr | Mixed-use podium carries higher OpEx than strip formats |

| Total Rent | $42–$60 psf/yr | Upper end reflects new CC4 podium product; lower end reflects older Central City inline |

| Demand Profile | Health · Wellness · F&B · Services | HBC liquidation creating re tenanting opportunity — large-format void likely to attract discount/off-price or entertainment concept |

| ── SOUTH SURREY / WHITE ROCK (PREMIUM) | ||

| Total Inventory | ~800,000 sf (est.) | Morgan Crossing · Semiahmoo · White Rock Square corridor |

| New Supply | Minimal | No new strip development; land and construction costs prohibitive |

| Vacancy Rate | ~1–3% | Tightest Surrey retail node; affluent demographics support strong occupancy despite tariff-related consumer caution |

| Net Asking Rate | $25–$42 psf/yr | Live LoopNet (Mar 2026): White Rock Square $25.00 psf (still active) · Redwood Square (King George) $42- $45 psf |

| Additional Rent | $12–$16 psf/yr | Institutional landlord (First Capital REIT, Re/Max) standard TMI |

| Total Rent | $37–$58 psf/yr | BC consumer resilient — outspending other provinces per capita (CBRE Jan 2026); South Surrey benefits from affluent demographics |

| Demand Profile | Specialty retail · F&B · Medical · Wellness | Lifestyle and daily-needs anchored formats outperforming; tariff-affected discretionary retail at more risk |

| ── NEIGHBOURHOOD / COMMUNITY STRIP | ||

| Total Inventory | ~3–4M sf (est.) | Newton · Whalley · Cloverdale · Guildford · Scott Road corridor |

| New Supply | Minimal | Retail vacancy tight across non-mall formats (2–4%); little new construction (CBRE Jan 2026) |

| Vacancy Rate | ~2–4% | Consistent with February 2026; strip/neighbourhood formats remain healthiest retail segment in Metro Vancouver |

| Net Asking Rate | $12–$28 psf/yr | Live LoopNet (Mar 2026): 10318-10324 Whalley Blvd $12.00 psf · Redwood Square $42–$45 psf (King George strip) |

| Additional Rent | $10–$14 psf/yr | Older strip centres carry lower operating costs than new mixed-use |

| Total Rent | $22–$42 psf/yr | Grocery/pharmacy-anchored formats strongest; retailers facing tariff cost pressure on discretionary goods most at risk (BMO Mar 2026) |

| Demand Profile | Grocery · Discount · F&B · Services | Everyday essentials and service-based retailers outperforming. Scott Road ethnic retail corridor benefits from resilient, diverse consumer base |

EXTERNAL MARKET FACTORS

The following Political, Economic, Environmental, Social, Technological and Legal factors are shaping the Surrey commercial leasing environment as of March 2026. Several factors have changed materially since the February 2026 report, most notably the BC Budget 2026 PST expansion, the US Supreme Court tariff ruling, and the advancing CUSMA review timeline.

| POLITICAL | – CUSMA scheduled for formal review July 1, 2026 — Canada-U.S. trade relationship at critical juncture. Canada has removed counter-tariffs on most U.S. goods (effective Sep 1, 2025) but steel, aluminum and automotive tariffs remain (EDC, Mar 2026). – US Supreme Court ruled (Feb 20, 2026) that IEEPA-based tariffs were illegal; Trump administration responded by invoking Section 122 of the 1974 Trade Act (10% tariff, 150-day maximum) and signalling intent to raise to 15%. Uncertainty remains the dominant theme. – PM Carney announced a $5-billion Strategic Response Fund for tariff- impacted sectors. ‘Buy Canadian’ federal procurement policy now mandates priority to domestic suppliers on contracts over $25M — potential boost to Surrey-based manufacturers. – BC Budget 2026: PST expanded to cover commercial real estate professional services (brokerage, property management, legal, accounting) effective Oct 1, 2026. Adds ~7% to transaction and management costs. (BLG, Mar 2026) – Surrey–Langley SkyTrain extension proceeding; City of Surrey pro-growth OCP update ongoing. Bill 44 upzoning near SkyTrain stations remains in effect. |

| ECONOMIC | – BoC policy rate held at 2.25% (Dec 2025). Three additional BoC rate cuts projected for 2026 by BMO Economics, totalling 75 bps. Lower rates improving development viability but tariff-driven inflation risk complicates BoC’s path. – BC GDP growth: B.C. government estimates tariffs could cause a cumulative $69B loss in provincial economic activity 2025–2028, with 124,000 job losses by 2028. BC Budget 2026 flagged as lacking measures to address looming construction decline (BCREA, Mar 2026). – Industrial rents expected to remain below $20 psf Jun 2025–Dec 2027 (Cushman & Wakefield Jun 2025). National industrial vacancy plateaued at 5.2% in Q4 2025 — potentially signalling an inflection point (JLL Feb 2026). – Metro Vancouver CRE investment volume: ~$9B in 2025 (down 14% YoY, Altus Group Q4 2025). Office investment up 92% driven by Pontegadea’s $1.2B acquisition of The Post. Retail up 31%. Industrial down 24%. – BC consumer more resilient than expected — outspending provincial counterparts per capita across major spending categories (CBRE Jan 2026). Retail fundamentals intact outside regional malls. |

| ENVIRONMENTAL | – BC Energy Step Code requirements increasing construction costs on new commercial builds. Tariffs on steel, aluminum (50%) and lumber (10%, rising) are further compounding cost inflation across all asset classes (JPMorgan Mar 2026). – City Centre 4 delivered LEED Gold — establishing new benchmark for sustainability requirements in Surrey AAA office. ESG ‘flight-to-quality’ pressure persisting; older Class B/C product facing rising compliance costs. – Campbell Heights: South Campbell Heights Local Area Plan approved by Surrey City Council (Dec 2024) — expanding the industrial zone with new ALR-compliant areas. Long-term supply relief but 3–5 year delivery horizon. – Construction material tariffs (steel 50%, aluminum 50%, lumber 10%+) adding materially to building costs, reinforcing decision to pause all speculative office projects and slow new industrial starts. |

| SOCIAL | – Surrey population 600,000+ — BC’s fastest growing city. Federal immigration cuts (2025–2027) moderating population growth pace but long- term demand thesis intact. – Return-to-office mandates from major employers and the federal government supporting positive suburban office absorption. Avison Young: 72% of professionals expect leasing activity to outperform in 2026. – Reduced federal immigration targets affecting education tenants — a key tech firm and education-sector occupier releasing space mid 2026 in Metro Vancouver (Avison Young Q4 2025). Watch for downstream impact on Surrey’s academic office cluster. – Tariff-driven economic uncertainty weighing on business confidence and leasing decisions. Tenants adopting ‘wait-and-see’ posture across industrial and office categories (JPMorgan Mar 2026). |

| TECHNOLOGICAL | – Surrey’s Health & Technology District now totals over ½M sf of AAA office — medtech, biotech and digital health cluster cementing its position as Metro Vancouver’s leading suburban health-tech precinct. – Flex/hybrid workspace norms continuing to reshape office fit-out requirements and space utilisation. TI allowances averaging $77.49 psf Metro Vancouver (Avison Young Q4 2025) as landlords invest in high- quality fit-outs to attract tenants. – E-commerce normalisation: global average tariff rate at 12% (Mar 10, 2026, Urban-Brookings Tax Policy Center). Higher tariffs on imported goods could reshape supply chains — near shoring and domestic manufacturing may benefit Metro Vancouver logistics. – Industrial automation demand continues driving requirements for higher clear heights, increased power capacity and modern mechanical specifications — most strongly seen in new Campbell Heights large-format stock. |

| LEGAL | – BC Budget 2026 PST expansion (effective Oct 1, 2026): PST at 7% will apply to brokerage commissions, property management fees, legal and accounting services used in commercial real estate. Significant new cost for buyers, vendors and operators (BLG Mar 2026). – CUSMA review scheduled July 1, 2026: formal renegotiation of Canada- US-Mexico Agreement could alter tariff structures materially. Key watch item for cross-border industrial and logistics tenants in Surrey’s Port Kells and Campbell Heights nodes. – US Supreme Court ruling (Feb 20, 2026): IEEPA tariffs struck down; Trump invoking Section 122 (10% tariff, 150-day limit). Ongoing legal volatility creating uncertainty for occupiers with cross border supply chains. – Bill 44 (Provincial): small-scale multi-unit zoning mandated near SkyTrainstations. OCP update in Surrey to reflect densification and mixed-use intensification along transit corridors. – HBC liquidation legal proceedings ongoing — largest single commercial tenancy risk in Surrey. Resolution of Central City anchor void is the key legal/leasing event to watch in Surrey retail through 2026. |

MARKET OUTLOOK

Office

Momentum is building but recovery will be uneven. Surrey City Centre is positioned to outperform the broader suburban market, benefiting from the Health & Technology District’s institutional anchor, SkyTrain access, and the absence of new competing supply. The vacancy trajectory should improve through 2026 as demand ticks up and no new supply arrives. Class A suburban parks face a longer recovery; landlords should expect continued pressure to offer higher TI packages and flexible terms for sub-5,000 sf tenants. The BC PST expansion on professional services (Oct 2026) will add incremental friction to transactions.

Industrial

The large-format segment is clearly tightening and approaching the point at which vacancy-driven rent pressure reverses. CBRE’s projection of large-format supply being cut in half by mid-2026 is the strongest near-term signal. Campbell Heights and Port Kells remain the premier nodes. Mid and small-bay product will lag, with recovery tied to SME confidence recovering as tariff uncertainty resolves and BoC cuts flow through. The tariff environment paradoxically supports medium-term rent recovery by suppressing new construction starts.

Retail

Non-mall retail in Surrey is stable and fundamentally healthy. The two defining events to watch through Q2–3 2026 are: (1) CC4 retail podium lease-up — pre-leasing progress and tenant mix will signal the direction of City Centre retail rents; and (2) HBC void resolution at Central City — re- tenanting with a discount, entertainment or fitness concept would be a positive signal for regional mall sentiment broadly. Grocery and pharmacy-anchored strip centres will continue to outperform. Tariff-exposed discretionary retailers face margin compression and potential footprint rationalisation.

Key Watch Items for Q2 2026

– CC4 retail podium pre-leasing progress and announced tenant mix (Q2 2026)

– HBC Central City void resolution — announcement of replacement anchor tenant

– CUSMA review launch (July 1, 2026) — initial negotiating positions from Canada, US and Mexico

– BC PST expansion (Oct 1, 2026) — budgeting impact on transaction costs and management fees

– BoC rate path — next decisions and forward guidance; critical for SME leasing confidence

– Industrial large-format absorption pace — CBRE’s mid-2026 supply halving prediction under observation

DATA SOURCES

This report draws on: CBRE Canada (Vancouver 2026 Outlook, Jan 21, 2026); Avison Young (Metro Vancouver Office Q4 2025); Cushman & Wakefield (Metro Van. Industrial Forecast, Jun 2025); JLL (Canadian Commercial Real Estate Outlook, Feb 2026); Altus Group (Vancouver CRE Q4 2025 Market Update); Borden Ladner Gervais LLP (BC Budget 2026 PST Analysis, Mar 2, 2026); CFIB (US Tariffs / CUSMA update, Mar 2026); Canada EDC (Canadian tariffs on US goods, Mar 5, 2026); JPMorgan (Tariffs and Commercial Real Estate, Mar 10, 2026); BMO (Canadian Commercial Real Estate Outlook, Mar 2026); Business in Vancouver (Feb 3, 2026); BCREA Housing Market Update (Mar 2026); LoopNet.ca active listings (accessed Mar–Apr 2026). Surrey- specific class-level vacancy rates remain estimated by triangulation from Metro Vancouver suburban averages and Surrey-specific listing data. Figures represent asking rents, not achieved rents.